When the global pulp and paper industry moves, we report it first — trusted by 8,000 subscribers across 80 countries

🏆 2026 Titan Analysis: Smurfit WestRock vs. Mondi

MARKET ANALYSIS

Jino John

2/9/20265 min read

The Battle of Scale vs. Science

📊 Executive Summary

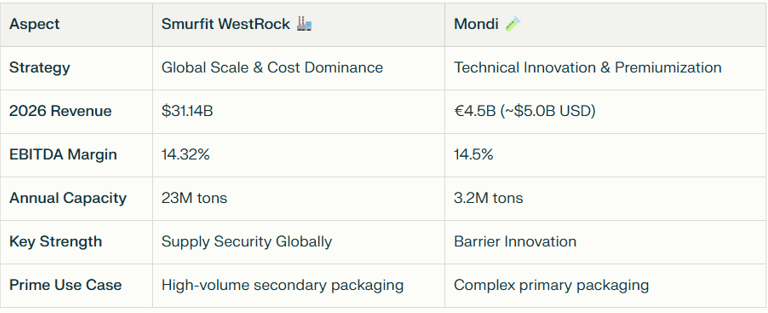

Two fundamentally different strategies dominate the fiber packaging world in 2026:

🏗️ SMURFIT WESTROCK (NYSE: SW) — The "Bellwether"

💪 STRENGTHS

🌍 Unmatched Scale

23M tons of annual containerboard capacity (world's largest)

Only player with top-tier positions simultaneously in:

North America (heartland of e-commerce)

Europe (mature but stable retail)

Latin America (fastest-growing region)

Achieved $31.14B revenue in trailing twelve months (Feb 2026)

🔒 Global "Supply Security"

14M tons of recovered fiber annually (60%+ of feedstock)

Insulated from commodity fiber shocks

Just-in-time production networks across 3 continents

Can fulfill Amazon/Walmart orders from any regional hub

⛓️ Vertical Integration

Controls the full value chain: tree → pulp → containerboard → converting

2024 merger created $400M+ cost synergy runway (on track by Q3 2026)

Eliminates middleman margin leakage

📈 Financial Momentum

Q1 2025: Adjusted EBITDA of $1.25B (16.4% margin) — significantly ahead of combined 2024

Net Debt/EBITDA down to a healthy 2.1x (Feb 2026)

Quarterly dividend: $0.43/share maintained despite integration costs

⚠️ WEAKNESSES

🔧 Integration Friction

Harmonizing two distinct corporate cultures (Irish Smurfit + US-based WestRock)

Legacy IT systems still being consolidated

Estimated $200-300M integration costs through end of 2026

Risk of key talent departures during restructuring

💰 Debt Stewardship

While improving, still carrying significant merger-related debt

Any sudden demand collapse (recession) could pressure covenants

Limited financial flexibility for opportunistic M&A or capex

🌐 Regional Concentration Risk

Heavy U.S. and Eurozone exposure = GDP cycle-dependent

If US consumer spending weakens (2026 prediction: muted 1-1.5% growth), volume suffers

Europe's energy crisis could ripple into cost structure

🚀 OPPORTUNITIES

💡 Synergy Capture

$400M+ cost savings from:

Mill network optimization (consolidating overlapping facilities)

Procurement leverage (15% + better terms on fiber/chemicals)

Technology sharing (best practices from both legacy companies)

Hit timeline: Full run-rate by Q2 2026

🎨 Premiumization

Moving beyond "brown box" commodity into:

EnShield® oil-resistant paperboards (luxury food/cosmetics)

High-graphic surface printing for retail visibility

Sustainable-certified grades commanding 5-15% price premiums

Target: 15-20% of revenue from premium grades by 2027

🌱 Emerging Market Expansion

India market growing at 15%+ CAGR (e-commerce, organized retail boom)

LatAm benefits from nearshoring (Mexico, Brazil replacing Asian sourcing)

Potential for greenfield mill investments if debt trajectory continues improving

🚨 THREATS

📉 Containerboard Oversupply

Global capacity expansions (China, SE Asia) may trigger "race to the bottom" on pricing late 2026

Analysts warn of 1-1.5% demand growth max but potential 3-5% new supply additions

Margin compression risk: 14.32% → 12-13% possible by Q4 2026

🤝 Buyer Power

Amazon, P&G, Unilever exert massive pricing pressure on high-volume contracts

Consolidated buyer base (top 10 customers = 40%+ of volume)

Lock-in risk: 3-year contracts with minimal price escalation

⚡ Energy Costs

EU energy volatility still a wild card (though improved vs. 2022-2023)

If European operations ramp to full utilization, exposure increases

🧪 MONDI GROUP (LSE: MNDI) — The "Agile Innovator"

💪 STRENGTHS

🏆 Barrier Innovation

9 WorldStar Awards in 2026 for solutions including:

re/cycle HiProtex: Paper + fiber composite replacing aluminum/plastic laminates

Moisture/oxygen barrier papers for coffee pouches, sterilizable medical packaging

Recyclable alternatives to BOPET films for snack food wrapping

First-mover advantage in functional fiber segment (5-10% of market, growing 8%+ CAGR)

🌱 Sustainability Leadership

83%+ of revenue now from eco-friendly/certified products

100% of portfolio is reusable, recyclable, or compostable

FSSC 22000 certified across all mills

Attracts ESG-focused brands (Unilever, Nestlé prefer Mondi solutions)

🎯 Strategic M&A Integration

Schumacher Packaging acquisition (2025) successfully integrated

Dominating European e-commerce + grocery subsegment

Cross-selling machine: Schumacher's customer base now accessing Mondi's barrier papers

Revenue synergies estimated at €50-100M+ annually

💰 Comparable Profitability

EBITDA margin of 14.5% — matching SW despite 1/6th the scale

Demonstrates pricing power for innovation-led solutions

Return on Capital Employed (ROCE): 11-12% (strong for paper sector)

⚠️ WEAKNESSES

📊 Profitability Volatility

Net margins more sensitive to ASP (average selling price) fluctuations for specific grades

Specialized paper grades have more volatile demand (fashion, food trends)

Less "cushion" from commodity volume contracts vs. SW

⚡ Energy Vulnerability

High concentration of European assets (70%+ of capacity)

EU energy grid shocks directly impact production costs

Carbon border adjustment mechanism (CBAM) creates rising regulatory costs

Less geographic diversification = higher operational leverage to energy prices

📈 Rising Leverage

Net debt-to-EBITDA rose to 2.5x in mid-2025 (post-Schumacher)

Higher than SW's 2.1x

Limited financial flexibility if economic conditions deteriorate

Dividend under pressure if margins contract

🚀 OPPORTUNITIES

🤖 Smart Packaging

AI, QR, RFID integration at scale to provide "Digital Identities" for every package

Track & trace solutions for supply chain transparency (regulatory tailwind in EU/US)

Data monetization: Mondi could sell supply chain insights to brands

TAM expansion: Potentially 50-100% premium pricing for "smart" vs. standard packaging

🌾 Non-Wood Fibers

Leading shift toward straw, bagasse, kenaf to lower costs in emerging markets

India, Brazil, SE Asia offer abundant agricultural residue feedstock

10-15% cost advantage vs. virgin/recycled fiber by 2028 (pilot mills ramping)

Regulatory tailwind: EUDR (EU Deforestation Regulation) makes alternative fibers attractive

🌏 Emerging Market Footprint

Currently underpenetrated in Asia/LatAm (vs. SW's presence)

High-graphic, barrier papers for beverage/FMCG brands in India, Indonesia

Acquisition pipeline for local converting assets (similar to Schumacher play)

🚨 THREATS

📋 EUDR Compliance

EU Deforestation Regulation adds high administrative costs to vast forestry operations

Requires traceability of all fiber inputs → supply chain audit burden

Non-compliance = exclusion from EU market (existential risk for 60%+ of revenue)

Estimated compliance cost: €50-100M+ through 2028

💊 "Plastic Pushback"

If fossil-fuel based plastic prices crash (oil downturn), cost-sensitive FMCG brands may slow fiber transition

Current fiber premium over plastic: 15-25%

Oil at $40/barrel would make plastic attractive again for cost-conscious CPG players

Risk to growth trajectory: Could slow barrier paper adoption to 3-5% CAGR (vs. current 8%+)

🏭 China Competition

Chinese fiber producers ramping scale in barrier papers

Labor + capital cost advantages = potential price wars by 2027-2028

Mondi's smaller scale means less ability to absorb margin pressure

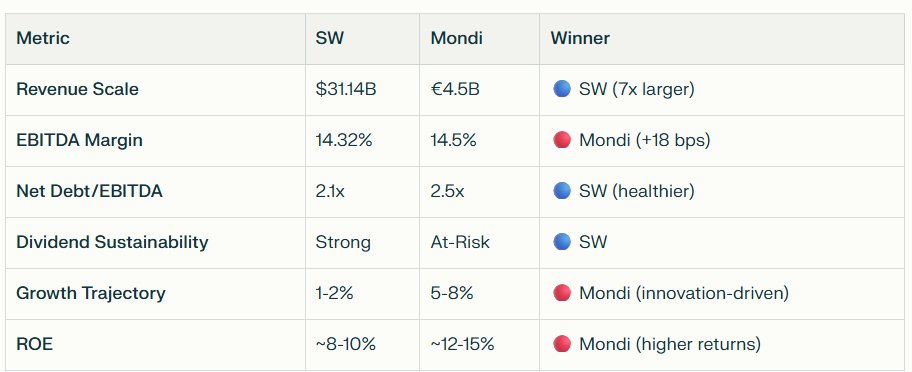

📊 DATA-DRIVEN COMPARISON

Financial Health Scorecard

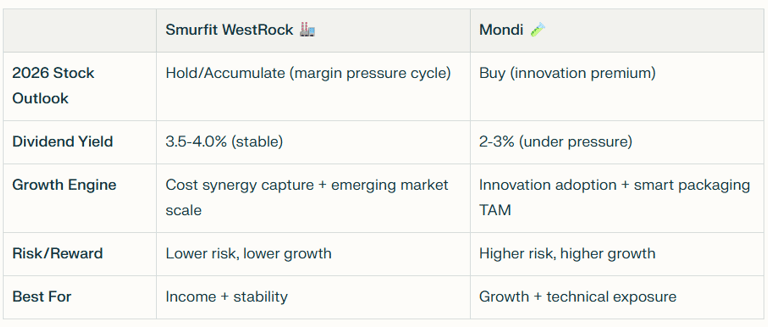

🎯 THE 2026 VERDICT

Choose Smurfit WestRock if you are:

✅ A global brand seeking supply resilience (multi-region fulfillment capability)

✅ Running high-volume secondary packaging (Amazon boxes, retail corrugated)

✅ Optimizing for lowest per-unit cost (commodity containerboard)

✅ Valuing production stability (massive scale = capacity buffers)

✅ An industrial buyer needing just-in-time logistics networks

The Utility of the Fiber World: Reliable, cost-optimized, globally available. Think "electricity grid"—you don't think about it, it just works.

Choose Mondi if you are:

✅ A premium brand requiring technical paper solutions (primary packaging)

✅ Needing moisture/oxygen barriers (coffee pouches, sterilizable medical wraps)

✅ Targeting ESG-conscious consumers (100% recyclable, certified solutions)

✅ Willing to pay 15-25% premium for innovation-led differentiation

✅ Seeking supply chain traceability (smart packaging, RFID integration)

The R&D Lab of the Fiber World: Cutting-edge, sustainable, technically sophisticated. Think "biotech firm"—continuous innovation, premium pricing, specialized solutions.

💡 Investment Thesis Summary

🔮 Watch These Catalysts in 2026

Smurfit WestRock

Q2 2026: Full $400M synergy run-rate announcement

Q3 2026: Container board pricing trends (capacity oversupply headwind?)

Feb 11, 2026: Medium-term investor update (full-year results)

Mondi

Feb 19, 2026: Q4 2025 earnings release (EUDR compliance cost disclosure)

Q2-Q3 2026: Smart packaging pilot wins (first revenue recognition)

H2 2026: Non-wood fiber mill ramp-up progress (India/Brazil)

🏁 Final Takeaway

2026 is the year of specialization in fiber packaging:

Smurfit WestRock wins the "commodity efficiency" battle through unprecedented scale

Mondi wins the "innovation premium" battle through first-mover technical leadership

Your choice depends on whether you value predictable, low-cost capacity or cutting-edge, sustainable solutions. Both are winners in their lanes. 🎯