When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

Europe Paper Industry Report – Q4 2025 (Based on Q4 & FY 2025 results of leading European producers)

MARKET ANALYSIS

Jino John

3/23/20262 min read

Executive Summary

The European paper and packaging industry remained in a prolonged downturn in Q4 2025, with weak demand, persistent pricing pressure, and structural oversupply.

Across all major producers—Billerud, Metsä Group, Mondi, Norske Skog, SCA, Stora Enso, and UPM-Kymmene—management commentary points to stable but low demand levels.

Pricing remained under pressure, particularly in containerboard and pulp, due to weak demand and capacity additions.

Margins compressed significantly, with some companies reporting losses or sharp EBITDA declines.

Cost relief (wood/pulpwood) began emerging late in the quarter, setting the stage for a cost-driven recovery in 2026.

1. Market Overview – Q4 2025

📉 Late-Cycle Conditions Persist

Q4 2025 confirms that the European paper industry is in a late downcycle phase, characterized by:

Weak macroeconomic environment

Low consumer confidence

Industrial slowdown

Continued supply-demand imbalance

Company confirmation:

Billerud → weak demand and oversupply

Stora Enso → demand stable at low levels

Mondi → no meaningful improvement

2. Demand Analysis (All 7 Companies)

Company-Level Demand Insights

Billerud

Weak demand in Europe & Asia

Oversupply intensifying

Packaging board volumes under pressure

Metsä Group

Price decline + weak demand → negative operating result

Mondi

Packaging volumes relatively resilient

No macro recovery

Norske Skog

Record deliveries driven by exports and ramp-up

SCA

Soft demand across segments

Stora Enso

Demand stable but low

UPM-Kymmene

Weak demand due to macro and geopolitical factors

🧠 Demand Conclusion

Demand across Europe in Q4 2025 remained weak to stable, with no broad-based recovery.

Volume stability in some segments is largely export-driven rather than demand-driven.

3. Pricing Trends

📉 Continued Pricing Pressure

Key observations:

Declines in:

Containerboard

Pulp

Wood products

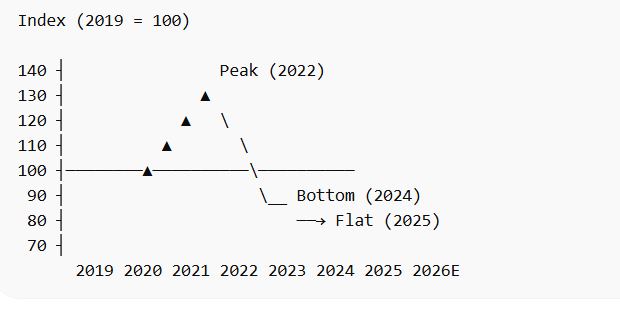

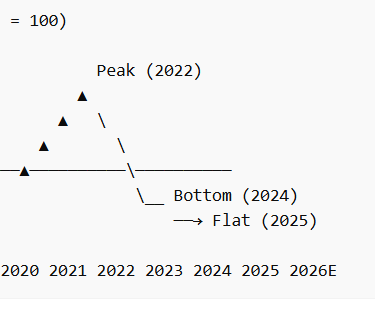

📊 Containerboard Pricing Trend (2019–2026E)

📊 Pricing Drivers

Oversupply

Weak demand

New capacity additions

Export competition

🔮 Q4 Insight

Pricing remained at or near cycle lows, with no clear upward momentum.

4. Cost & Margin Dynamics

⚡ Cost Trends

Positive developments:

Pulpwood prices ↓ ~20% from peak → Billerud

Negative factors:

Energy costs still elevated

Carbon costs increasing

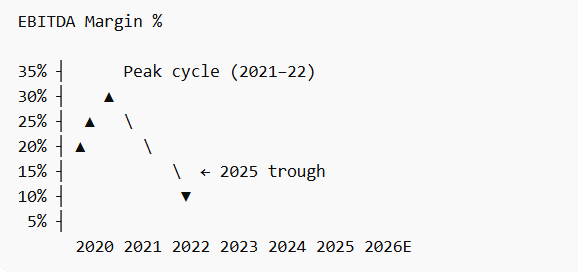

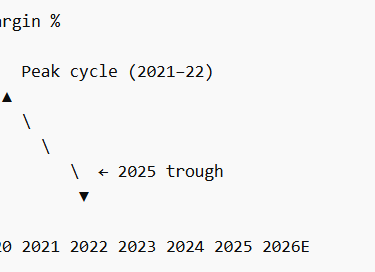

📊 EBITDA Cycle Trend

🧠 Margin Insight

Q4 2025 represents a cyclical profitability trough, with margins compressed across nearly all producers.

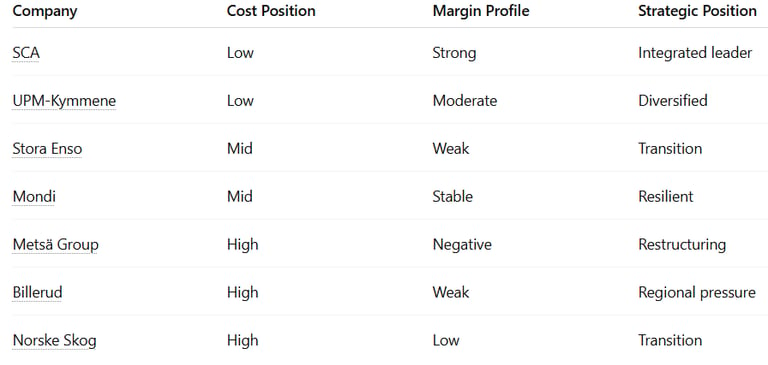

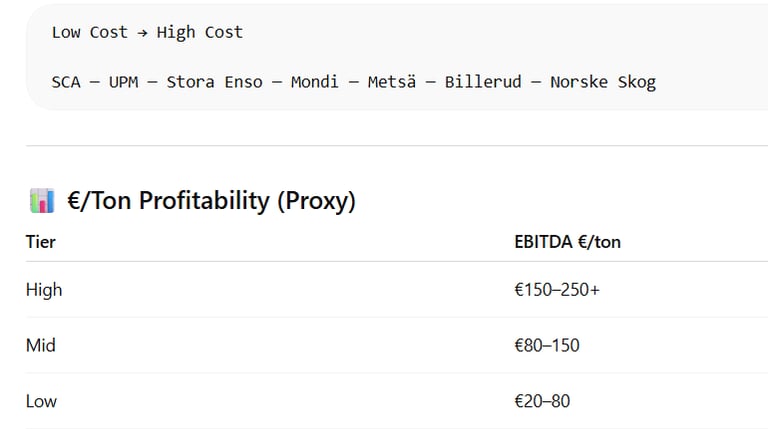

5. Competitive Positioning & Benchmarking

📊 Company Benchmarking Table

6. Supply & Capacity Dynamics

📦 Oversupply Continues

New capacity additions

Ramp-ups impacting pricing

🔄 Restructuring

Closures → UPM-Kymmene

Workforce cuts → Metsä Group

Site rationalization → Mondi

7. Sustainability & ESG

🌱 Key Trends

Decarbonization

Circular packaging

Renewable fibre

8. Key Risks

Weak macro environment

Overcapacity

Energy volatility

Export dependence

9. Q4 2025 → 2026 Outlook

🔮 Key Signals

Positive:

Wood costs declining

Cost-saving programs

Negative:

Weak pricing

No demand recovery

🧠 Final Analyst Conclusion

“Q4 2025 confirms that the European paper industry remains in a late-cycle downturn, with weak demand, persistent pricing pressure, and compressed margins. Recovery in 2026 will be driven primarily by cost normalization rather than demand growth.”