When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

European Publication Paper Market Structural Overcapacity, Corporate Restructuring & Strategic Realignment in the Magazine Paper Segment

MARKET ANALYSIS

Jino John

5/16/202611 min read

1. Executive Summary

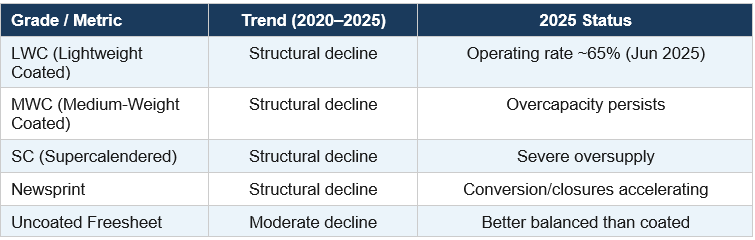

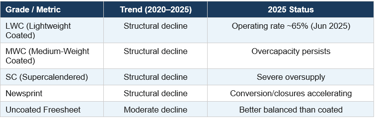

The European publication paper sector is in the midst of its most consequential structural reorganisation in decades. Persistent and deepening overcapacity in the magazine paper segment — spanning lightweight coated (LWC), medium-weight coated (MWC), and supercalendered (SC) grades — is driving an unprecedented wave of mill closures, capacity conversions, and corporate consolidation that is reshaping the competitive landscape across the continent.

Demand for European graphic paper has declined by an estimated 30–40% over the past decade, accelerated by the irreversible migration of advertising budgets and readership to digital platforms. In June 2025, Western European graphic paper demand fell by a further 10% year-on-year, pushing LWC operating rates to approximately 65% — a level structurally incompatible with long-term mill viability. Despite the removal of more than one million tonnes of annual production capacity between 2023 and 2025, the supply–demand gap remains wide.

The defining corporate development of the current cycle is the proposed 50/50 joint venture between UPM-Kymmene and Sappi, announced in December 2025 and valued at a combined €1.42 billion. This transaction — currently under Phase II EU merger control review — would create the largest graphic paper entity in Europe and represents an acknowledgement by the industry’s two leading participants that standalone survival in the current environment is not viable. Simultaneously, Norske Skog and Stora Enso have executed major capacity conversions from publication to packaging grades, while Sappi, Heinzel, and Kabel Premium Pulp & Paper have executed or announced permanent mill closures.

The outlook for the segment remains deeply challenging. Unless capacity is removed significantly faster than demand erosion, operating rates will remain structurally depressed, suppressing producer economics and threatening the long-term viability of a stable European supply base for magazine publishers and commercial printers.

Key Finding

Even after all announced closures are implemented, LWC market operating rates are projected to remain below 82% in early 2026 and will likely deteriorate further as demand continues its structural decline. Further decisive capacity action is required to restore sustainable market balance.

2. Market Overview

2.1 Demand Dynamics

European publication paper demand has been in secular decline since approximately 2007, driven by the long-term contraction of the print advertising market and the structural shift of media consumption from print to digital channels. The pace of decline has accelerated materially since 2020, reflecting the post-pandemic consolidation of digital habits, the collapse of consumer magazine advertising revenues, and ongoing print circulation declines across all major European markets.

CEPI member countries recorded a 12.8% decline in paper and board production in 2023 relative to the prior year — one of the steepest annual declines on record — driven by high inflation, elevated interest rates, weakened private consumption, and destocking by downstream customers. Across LWC, MWC, and SC grades, demand contraction has been consistent and shows no credible signs of reversal.

2.2 Supply & Capacity

Production capacity in the magazine paper segment has contracted significantly since 2020, but capacity removal has consistently lagged the rate of demand erosion. The resulting operating rate depression — with LWC running at approximately 65% as of mid-2025 — has suppressed transaction prices, compressed margins, and undermined producers’ ability to invest in sustainability and product development.

Industry forecasters note that even a hypothetical step-change closure of all currently announced capacity would lift LWC operating rates from ~65% to only ~82% — still below the threshold generally considered necessary for pricing discipline and sustainable producer economics. Given continued demand erosion, the effective operating rate recovery is likely to undershoot even this modest improvement.

Overcapacity in Context

The publication paper market’s overcapacity is structurally distinct from cyclical overcapacity in other grades. Unlike packaging or tissue, where demand recovers with the economic cycle, magazine paper demand reflects a one-way substitution to digital. Capacity rationalisation is therefore a permanent adjustment, not a cyclical correction.

2.3 Cost Environment

Europe’s cost position in global paper production has deteriorated dramatically over the past five years. A recent Rabobank report noted that Europe has transitioned from one of the lowest-cost paper-producing regions globally to the highest-cost, primarily driven by energy price inflation following the geopolitical disruption to European gas markets since 2022. Electricity and fuel costs represent a disproportionately large share of the cost base for energy-intensive mechanical paper grades such as LWC and SC.

Rising carbon costs under the EU Emissions Trading System (ETS), alongside the upcoming introduction of ETS 2, add further structural cost pressure. These factors compound the economic unviability of high-cost, lower-utilisation mill assets, accelerating closure timelines.

3. Mill Closures & Capacity Withdrawals

Kabel Premium Pulp & Paper – Hagen, Germany

Capacity Removed: ~450,000 tpa

Grade: LWC / coated mechanical

Status: Permanent closure

Sappi – Stockstadt, Germany

Capacity Removed: ~220,000 tpa

Grade: Coated & uncoated woodfree

Status: Closed Q1 2024

Sappi – Kirkniemi PM2, Finland

Capacity Removed: ~175,000 tpa

Grade: Coated mechanical / LWC

Status: Permanent PM closure

UPM – Ettringen, Germany

Capacity Removed: ~270,000 tpa

Grade: SC / improved newsprint

Status: Permanent closure

UPM – Kaukas PM1, Finland

Capacity Removed: ~300,000 tpa

Grade: LWC / coated mechanical

Status: Permanent shutdown

Heinzel – Laakirchen, Austria

Capacity Removed: Undisclosed

Grade: SC / uncoated mechanical

Status: Publication paper ceased

French sector-wide closures

Capacity Removed: Multiple

Grade: Mixed grades

Status: 7+ mills closed since 2024

Major Publication-to-Packaging Conversions

Norske Skog – Golbey, France

235k tpa newsprint removed; 550k tpa containerboard added

Norske Skog – Bruck, Austria

125k tpa newsprint converted to recycled containerboard

Stora Enso – Langerbrugge, Belgium

Newsprint converted to 700k tpa testliner/fluting

Stora Enso – Oulu, Finland

Former publication paper assets converted to consumer board

UPM–Sappi Joint Venture

The proposed UPM–Sappi joint venture represents the defining strategic restructuring event in the European publication paper industry. The transaction combines UPM Communication Papers with Sappi Europe’s graphic paper operations into a 50/50 joint venture valued at approximately €1.42 billion enterprise value.

The joint venture is widely expected to accelerate additional machine closures and capacity rationalisation across Germany, Finland, and other high-cost regions.

4.Divestitures, Acquisitions & Corporate Restructuring

4.1 Stora Enso: Strategic Exit from Publication Paper

Stora Enso, the Finnish-Swedish forest industry conglomerate, has executed the most comprehensive strategic exit from publication paper of any major European producer. In March 2022, the company initiated a formal sales process for four of its five European paper production sites, retaining only Langerbrugge for conversion to packaging. The process reflected Stora Enso’s determination to reposition its portfolio entirely around packaging, biomaterials, and wood products.

In April 2023, Stora Enso completed the divestment of its Swedish paper production site for €18 million — a modest consideration that illustrates the depressed asset values prevailing in the European publication paper sector. Further site disposals have followed as part of the programme. In parallel, Stora Enso has launched a strategic review of its Central European sawmills and building solutions operations, with divestment identified as one potential outcome.

On the packaging side, Stora Enso agreed to divest its German corrugated packaging plants to Dunapack Packaging, the corrugated packaging division of the Prinzhorn Group, in a transaction announced in April 2025. This divestment reflects Stora Enso’s tightening strategic focus on consumer packaging (centred on the Oulu investment) and biomaterials, rather than corrugated packaging, as its primary growth platforms. From 2026, Stora Enso is consolidating its business reporting into Consumer Packaging, Integrated Packaging, Biomaterials, and Other segments to reflect its packaging-focused operating model.

4.2 UPM–Sappi Joint Venture: The Industry’s Defining Transaction

The most consequential corporate development in the European graphic paper market — potentially in the industry’s modern history — is the proposed 50/50 joint venture between UPM-Kymmene Corporation and Sappi Limited, announced on 4 December 2025 through the signing of a non-binding letter of intent.

4.2.1 Transaction Structure and Rationale

The proposed joint venture would combine UPM’s entire Communication Papers business with Sappi’s European graphic paper operations into a single independent company, held 50/50 by the two parent groups. The combined enterprise value of the contributed businesses is €1.42 billion (excluding anticipated synergy benefits), with UPM’s business valued at €1.1 billion and Sappi’s European graphic paper assets at €320 million. The transaction would be structured as a debt-financed acquisition by the joint venture company of assets contributed by each parent.

UPM would receive cash proceeds of €613 million and a 50% shareholding in exchange for its Communication Papers business. Sappi would receive €139 million in cash and a 50% shareholding. The joint venture’s dividend policy would distribute all excess cash to shareholders. The transaction structure is designed to enable potential future divestment of either party’s shareholding three years post-closing once integration is complete and synergies realised.

4.2.2 Assets Contributed

From UPM: the entire Communication Papers business, comprising eight paper mills including Augsburg and Schongau (Germany), Nordland PM1 and PM4 (Germany), Rauma including UPM RaumaCell (Finland), Kymi (Finland), Jämsänkoski PM6 (Finland), the Caledonian mill (United Kingdom), and the Blandin mill in Grand Rapids, Minnesota (USA). UPM’s Communication Papers business generated approximately €2.9 billion in annual turnover.

From Sappi: the European graphic paper business, comprising four mills — Gratkorn (Austria), Ehingen (Germany), Maastricht (Netherlands), and Kirkniemi (Finland). Kirkniemi, described as the world’s largest coated publication paper mill with a capacity of approximately 750,000 tpa, is the most strategically significant Sappi asset in the transaction. Sappi’s contributed businesses generated EBITDA of €64 million on turnover of approximately €1.5 billion in the 12 months to September 2025.

4.2.3 Rationale and Expected Benefits

Both UPM and Sappi’s leadership have been explicit that the joint venture is a “decisive response to the structural changes in the European graphic paper industry.” The transaction is expected to generate operational synergies of at least €100 million per annum through the reallocation of production volumes to the most efficient machines, fixed cost elimination, and procurement benefits. These synergies are the primary financial rationale, given the structurally declining underlying market.

The deal also enables UPM to substantially reduce its exposure to the graphic paper segment, freeing capital for redeployment into higher-growth businesses including UPM Specialty Papers and UPM’s biofuels and biochemicals operations. For Sappi, the transaction delivers on its Thrive25 strategy to reduce direct graphic paper exposure and reposition toward packaging, specialty papers, pulp, and biomaterials.

4.2.4 Regulatory Status

The European Commission initiated a Phase II merger control investigation on 28 April 2026 following the conclusion of Phase I without a full resolution of initial concerns. Phase II investigations are standard in complex concentration cases and do not preclude approval. UPM and Sappi continue to engage constructively with the Commission. Definitive agreements remain targeted for the first half of 2026, with transaction close expected by end-2026, subject to European Commission and other jurisdictional approvals (including the UK, US, and China) and Sappi shareholder approval.

Scale of the UPM–Sappi JV

The combined entity, once formed, would command a substantial share of European graphic paper capacity across woodfree coated, uncoated freesheet, and coated mechanical segments. European demand for woodfree coated and uncoated paper alone was estimated at approximately 8.5 million tonnes in 2025. The JV’s ability — and willingness — to rationalise capacity decisively will be the critical variable determining whether the European market achieves structural rebalancing.

4.3 Lecta Group: Recapitalisation and Specialty Repositioning

Spanish paper group Lecta completed a recapitalisation process in early 2025, having undergone financial restructuring following periods of market stress. The company considers itself better positioned following the recapitalisation, both financially and organisationally, and is targeting a long-term transformation toward specialty paper supply — particularly in areas such as self-adhesive papers, release liners, and functional papers — where demand dynamics are more favourable than in commodity graphic grades.

4.4 International Paper – DS Smith: Packaging Consolidation

While not a direct publication paper transaction, the acquisition of UK-headquartered DS Smith by US packaging giant International Paper — a deal with a combined pro-forma 2023 revenue of approximately $28.2 billion and anticipated annual cash synergies of at least $514 million — has material implications for European paper flows. The integration of IP and DS Smith is expected to generate approximately 600,000 short tons of annual operational benefit, and could affect the volume of European uncoated freesheet exports to North America, as European coated paper producers capable of grade-switching may redirect volumes. The acquisition reinforces the broader industry narrative of consolidation and scale as the primary strategic response to structural overcapacity and cost pressure.

5 Grade Diversification by Incumbent Producers

A number of publication paper producers that have chosen not to close or convert assets outright have instead pursued grade diversification strategies, adding new product lines to their existing publication paper mills in order to offset declining volumes and improve utilisation rates.

5.1 Sappi — Kirkniemi (Finland)

Sappi has commenced production of uncoated mechanical book paper grades at its Kirkniemi mill in Finland, alongside its core coated publication paper output. This move, which mirrors a similar initiative at Norske Skog’s Skogn mill in Norway, reflects an attempt to access the more stable book paper segment as an incremental demand source within existing mill infrastructure.

5.2 Norske Skog — Skogn (Norway)

Norske Skog has introduced uncoated mechanical book paper production at its Skogn mill in Norway, diversifying away from its traditional newsprint and publication paper grades into a segment with relatively more stable structural demand. Book publishing, while not immune to digital competition, has demonstrated greater resilience than consumer magazine or newspaper publishing, providing a degree of portfolio stabilisation.

5.3 UPM Specialty Papers

UPM has been systematically building its Specialty Papers division as a strategic counterweight to its declining Communication Papers exposure. The division produces labelling, packaging, and release liner papers, and has benefited from growing regulatory pressure to replace plastic-based packaging with paper alternatives. UPM Specialty Papers and Royal Vassen announced a partnership in late 2025 to develop recyclable and food-safe barrier paper solutions for dry product packaging.

5.4 Sappi Packaging & Specialties (Europe)

Sappi Europe has expanded its packaging and specialties portfolio as the primary growth vector under its Thrive25 strategy. Target segments include flexible packaging papers, functional papers, self-adhesives, glassine, labels, and dye-sublimation papers. In September 2025, Sappi launched its Guard Pro OHS and Guard Pro OMH mono-material papers — recyclable products delivering high-barrier protection against oxygen, water vapour, grease, and MOSH/MOAH contamination — as part of its packaging growth agenda.

6. Outlook and Strategic Implications

6.1 Near-Term Market Outlook

The near-term outlook for the European magazine paper segment remains adverse. Demand is forecast to continue declining at a rate of 6–10% annually depending on grade, driven by ongoing structural pressures rather than cyclical factors. Operating rates in the LWC segment are unlikely to recover materially above 80% in 2026 without further capacity withdrawal beyond what has already been announced, and may deteriorate further if the pace of conversion and closure actions moderates.

The finalisation and implementation of the UPM–Sappi joint venture will be the most significant determining factor in the short-term supply–demand balance. The JV’s stated objective of reallocating volumes to the most efficient machines implies deliberate capacity rationalisation — but the quantum, pace, and permanence of that rationalisation will be critical. If the JV opts for modest rationalisation to maintain volume and market share, operating rates will remain depressed. If it pursues aggressive capacity removal consistent with restoring structural balance, the market could begin to stabilise.

6.2 Risk Factors

The following risk factors could further destabilise the publication paper market in the near to medium term:

• EU Merger Control: A Phase II investigation into the UPM–Sappi JV creates uncertainty. If the European Commission requires significant asset disposals as a condition of approval, the JV’s rationalisation capacity may be constrained.

• Import Competition: Increased exports of coated paper from Asian and South American producers, capitalising on European demand for competitively priced alternatives amid supply tightening, could undermine any recovery in producer pricing power.

• Energy Cost Volatility: Elevated and unpredictable energy prices continue to compress margins and create barriers to investment in conversion or sustainability projects. The war premium embedded in European energy markets adds an additional layer of unpredictability.

• Demand Acceleration: The pace of digital substitution could accelerate beyond current forecasts, particularly if remaining major magazine publishers reduce pagination or frequency more aggressively than anticipated.

• Disorderly Closure: The financial stress of several producers creates a risk of abrupt, unplanned mill closures that could disrupt supply chains and leave publishers without adequate supply on short notice.

6.3 Strategic Recommendations

For producers, the strategic imperatives are clear: accelerate capacity rationalisation, invest in conversion to packaging or specialty grades where assets are competitive, and pursue consolidation where standalone viability is in question. The UPM–Sappi JV model — combining scale, synergy realisation, and eventual divestment flexibility — provides a template for others to consider.

For publishers and print buyers, the risk of supply disruption is real and growing. Strategic procurement approaches, including longer-term supply agreements with the most financially resilient producers, are advisable. The gradual disappearance of capacity in specific uncoated mechanical grades (particularly those with specific printing qualities valued by high-end magazine publishers) is already generating buyer nervousness and warrants active supply chain risk management.

For policymakers and industry bodies, the case for coordinated restructuring support — including worker transition programmes, conversion investment support, and strengthened trade defence measures against unfair import competition — is compelling. A disorderly market collapse in publication paper would have wider consequences for the European commercial printing, publishing, and media ecosystems.

Looking Ahead

The European publication paper market is at an inflection point. The structural forces driving decline are irreversible. The question is not whether the market will contract further, but whether that contraction will be managed in an orderly manner that preserves a viable, competitive European supply base, or whether it will be characterised by financial distress, disruptive closures, and supply insecurity for downstream customers.