When the global pulp and paper industry moves, we report it first — trusted by 7,000 subscribers across 80 countries

FUJIAN PROVINCE PAPER INDUSTRY 2025 ANNUAL REVIEW & STRATEGIC OUTLOOK

MARKET ANALYSIS

Jino John

4/1/20269 min read

Executive Summary

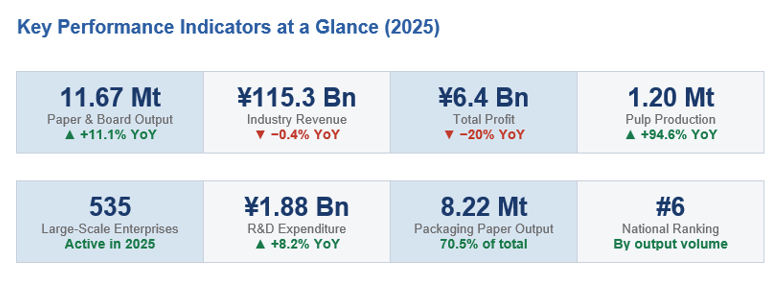

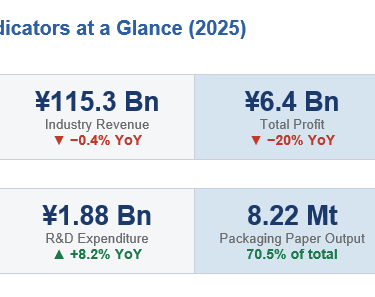

Fujian Province's paper industry delivered a record 11.67 million tons of machine-made paper and paperboard in 2025 — an 11.1% increase year-on-year — ranking the province sixth nationally. This output milestone was achieved against a backdrop of structural headwinds: weak domestic demand, persistent overcapacity across low-value grades, and elevated input costs compressed total industry profit by approximately 20% to RMB 6.4 billion.

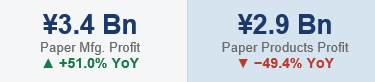

The divergence between sub-sectors was stark. Paper manufacturing enterprises grew profits by 51%, while paper product manufacturers saw profits collapse by 49.4%. Pulp production surged 94.6%, reflecting new integrated capacity coming online. Industry concentration accelerated — four enterprises alone account for 65.4% of total provincial output — and three companies have crossed the 1 million-ton production threshold.

Looking ahead to 2026, Fujian's paper industry is transitioning from volume-driven expansion to value creation — driven by specialty paper growth, digital transformation, green manufacturing standards, and deepening regional cluster development across Sanming, Quanzhou, and Zhangzhou.

1. Production Performance

1.1 Overview of Output Growth

Fujian Province completed production of 11.6656 million tons of machine-made paper and paperboard in 2025, representing an 11.1% year-on-year increase and placing the province sixth among all Chinese provinces by output volume. This growth rate significantly outpaced China's national average, which stood at approximately 2.7% for the January–August 2025 period according to Zhiyan Consulting, highlighting Fujian's expanding share of domestic production capacity.

The industry's enterprise base comprised 535 large-scale entities: 2 pulp manufacturers (unchanged), 116 paper manufacturers (down 4 year-on-year), and 417 paper product manufacturers (up 1). The slight contraction in paper manufacturing entities reflects ongoing consolidation among smaller players unable to compete against integrated, large-scale operations.

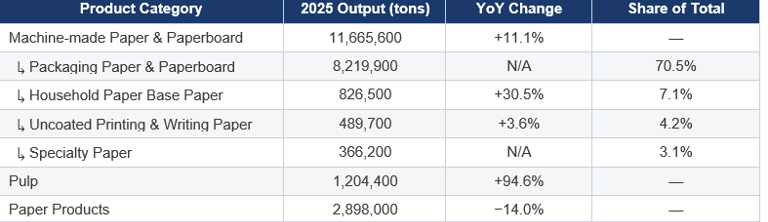

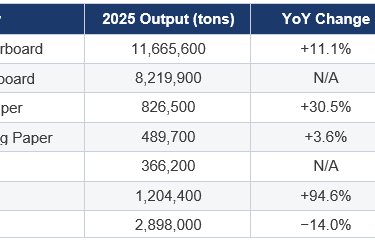

1.2 Production by Category

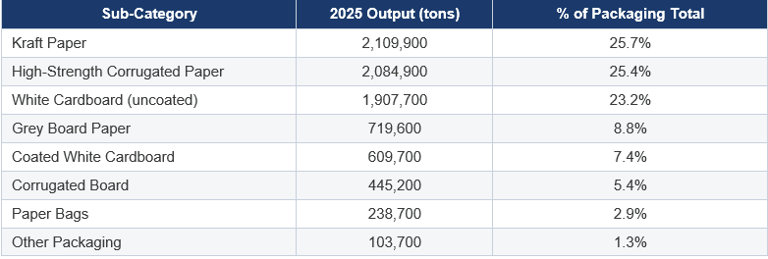

1.3 Breakdown of Packaging Paper & Paperboard

Packaging paper and paperboard — the backbone of Fujian's paper industry — totaled 8.22 million tons in 2025, accounting for roughly 70% of total machine-made paper output. The sub-category composition is detailed below:

The dominance of kraft paper, corrugated media, and white cardboard reflects Fujian's strong positioning in the e-commerce and industrial packaging supply chain. National data from Mordor Intelligence confirms that corrugated boxes commanded 35.6% of China's paper packaging market share in 2025, driven by sustained growth in express freight and online retail, reinforcing demand for exactly these grades.

1.4 Pulp Production Surge

The near-doubling of pulp output — from approximately 619,000 tons in 2024 to 1,204,400 tons in 2025 (+94.6%) — marks a structural inflection point. This reflects major new integrated pulp-paper capacities coming online at leading enterprises such as Liansheng Pulp & Paper (Zhangzhou) Co., Ltd. The shift toward integrated production is a proven strategy for managing raw material costs, reducing dependency on volatile global pulp markets, and improving gross margins — mirroring the approach taken by national leaders such as Nine Dragons Paper and Sun Paper Group.

2. Financial Performance & Profitability

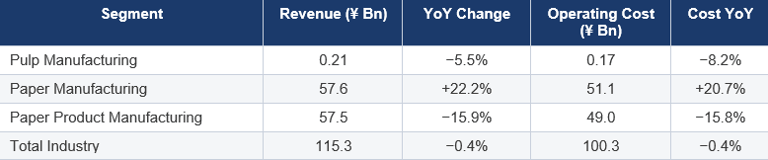

2.1 Revenue and Cost Dynamics

Total industry operating revenue was approximately RMB 115.3 billion in 2025, a marginal decline of 0.4% year-on-year. Despite flat revenue at the top line, underlying structural divergence between sub-sectors was pronounced. Paper manufacturing revenue rose 22.2% to RMB 57.6 billion, while paper product manufacturing revenue declined 15.9% to RMB 57.5 billion — almost exactly canceling each other out in aggregate.

The near-parallel movement of revenues and costs across all segments indicates that margin improvement — not cost reduction — was the primary driver of profit differentiation. Paper manufacturers succeeded in widening margins, while paper product manufacturers faced a demand-driven revenue collapse that reduced gross margins significantly despite corresponding cost cuts.

2.2 Profitability Analysis

Total industry profit declined approximately 20% to RMB 6.4 billion. However, this figure masks sharply divergent trajectories:

The paper product manufacturing segment's 49.4% profit collapse was the primary driver of industry-level profit deterioration. This reflects the combined effect of overcapacity in corrugated boxes and other converted products, a slowdown in downstream manufacturing orders, and rising competition from packaging producers in other provinces. The sales-to-production ratio across the industry stood at 90.91%, indicating a moderate but meaningful inventory overhang that will require destocking in 2026.

2.3 R&D Investment Trends

Total industry R&D expenditure reached RMB 1.88 billion in 2025, up 8.2% year-on-year — a positive signal that enterprises are investing through the current earnings trough to build long-term competitive positioning. Notably, pulp manufacturers led in relative growth (+42.9%), though off a small base. Paper manufacturing R&D rose 19.1%, while paper products R&D contracted slightly (−1.9%), consistent with margin pressure in that segment.R&D is increasingly focused on specialty papers and specialty pulp — product categories that typically carry higher gross margins and serve fast-growing end-markets such as lithium battery separators, food-grade functional packaging, and pharmaceutical applications.

3. Enterprise Landscape & Market Concentration

3.1 Concentration Is Accelerating

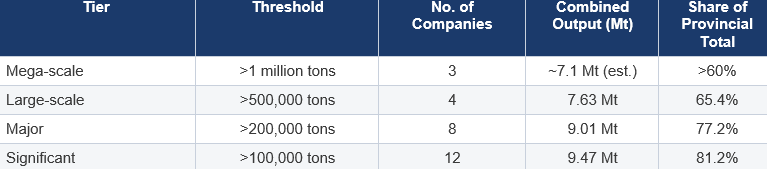

One of the most significant structural features of Fujian's paper industry in 2025 is the rapid acceleration of market concentration. The data below illustrates how a handful of enterprises dominate provincial output

Three companies have crossed the 1 million-ton production threshold: Liansheng Paper (Longhai) Co., Ltd., Liansheng Pulp & Paper (Zhangzhou) Co., Ltd., and Nine Dragons Paper (Quanzhou) Co., Ltd. This ultra-high concentration at the top of the production pyramid — typical of mature industrial economies — is a relatively recent development in Chinese papermaking and signals that Fujian is ahead of the national curve in industry rationalization.

3.2 Top 10 Paper & Paperboard Producers (2025)

Three companies — Fujian Youxi Yongfengmao Paper Co., Ltd., Shanying South China Paper Co., Ltd., and Fujian Lishu Group — recorded production increases exceeding 10% in 2025, demonstrating that capacity additions by second-tier players continue even as overall profit conditions tighten.

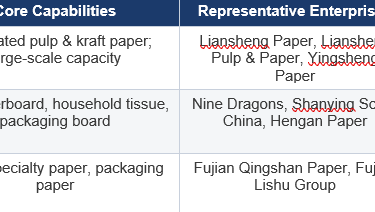

3.3 High-Performing Enterprises

Among large-scale paper manufacturing enterprises assessed by the Fujian Paper Industry Association, four companies stood out for financial resilience and operational performance:

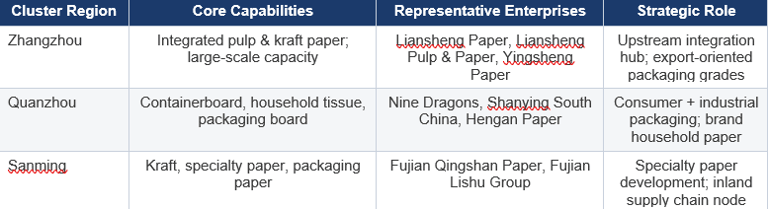

4. Regional Industrial Clusters

Paper-making capacity in Sanming, Quanzhou, Zhangzhou, and surrounding regions collectively accounts for more than 80% of Fujian Province's total paper production capacity, forming three distinct but complementary industrial clusters:

The spatial concentration of production in these three regions creates significant logistics efficiencies, shared supplier ecosystems, and talent pools — advantages that reinforce the competitive moat of Fujian-based enterprises relative to more dispersed provincial competitors. These clusters are expected to deepen further in 2026 as leading enterprises continue to optimize their capacity and product structure layouts within established industrial zones.

5. National & Global Market Context

5.1 China's Paper Industry — National Perspective

China's paper and paperboard manufacturing market was valued at USD 211.3 billion in 2025, representing a CAGR of 4.8% over the preceding five years (IBISWorld). From January through August 2025, China's national machine-made paper and paperboard output reached 106.66 million tons, a 2.7% year-on-year increase (Zhiyan Consulting). Fujian's 11.1% growth rate therefore represents a significant outperformance versus the national benchmark.

Nationally, Shandong, Guangdong, Zhejiang, and Jiangsu have historically ranked as the largest paper-producing provinces by enterprise count and output. However, Fujian has distinguished itself through rapid capacity scale-up, integrated supply chains, and a relatively concentrated enterprise structure dominated by a small number of ultra-large operators.

5.2 Structural Overcapacity — An Industry-Wide Challenge

Overcapacity is not a Fujian-specific challenge but a defining feature of China's paper industry. According to ResourceWise analysis published in October 2025, China has added more than 25 million tons of containerboard capacity since 2019 — with operating rates remaining in the 60–80% range across the industry. This structural imbalance has created a global price-ceiling effect, compressing margins for Western competitors and intensifying competition within domestic markets.

For Fujian enterprises, the strategic response has been two-fold: scale consolidation at the top end (where per-unit costs are lowest), and product premiumization in specialty papers and high-value household grades where overcapacity pressures are less acute.

5.3 China's Paper Packaging Market Outlook

China's paper packaging market was valued at USD 91.75 billion in 2025 and is projected to grow at a 4.77% CAGR through 2031, reaching USD 121.31 billion (Mordor Intelligence). Key demand drivers include:

• E-commerce parcel volume growth, which drives sustained demand for corrugated and kraft packaging grades — Fujian's largest output categories.

• Government plastic-reduction mandates under the 2025 'Green Packaging' regime, accelerating substitution of plastic mailers and single-use items with paper-based alternatives.

• Extended Producer Responsibility (EPR) schemes incentivizing recycled-fiber content, benefiting integrated mills with OCC (old corrugated containers) processing capabilities.

• Food and beverage sector demand — food applications commanded 41.1% of China's paper packaging market in 2025.

6. Green Transformation & Sustainability

6.1 Regulatory Framework

China's 'Dual Carbon' strategy — targeting carbon emission peak before 2030 and carbon neutrality before 2060 — is creating concrete pressure on the paper industry to reduce emissions intensity. China's national emissions-trading scheme (ETS) now covers 4.5 billion tons of CO2, and rising utility tariffs under dynamic pricing are compressing profitability for energy-intensive virgin-fibre operations.

The 2025 amendment to the Express Delivery Regulations mandates that couriers prioritize recyclable or biodegradable materials, directly stimulating demand for paper-based packaging over plastic. The mandatory standard GB 43352-2023 (effective June 2024) caps heavy-metal levels in express packaging, raising entry barriers for smaller, less technologically advanced converters.

6.2 Industry Response — Fujian's Green Positioning

Fujian's paper enterprises increased total R&D investment to RMB 1.88 billion in 2025, with a meaningful proportion directed toward green manufacturing technologies and specialty product development. Key green transformation trends include:

• Integrated pulp capacity expansion reducing dependency on imported fiber and lowering Scope 3 emissions through supply chain shortening (most notably at Liansheng Pulp & Paper).

• Digital and intelligent manufacturing adoption accelerating across leading enterprises, improving energy efficiency, waste reduction, and production yield per ton of input.

• Specialty paper development in high-margin applications including water-based barrier food packaging — aligned with China's plastic restriction mandates and the global zero-PE lamination trend that reached large-scale commercial production at Shandong Bohui in February 2025.

• Circular economy integration: nationally, recycled fiber captured 63.1% of China's paper packaging market in 2025 as state targets steer mills toward lower-emission furnish mixes (Mordor Intelligence). Fujian's integrated producers are well-positioned to benefit from this structural shift.

• Carbon footprint transparency is becoming a procurement prerequisite as lead buyers embed carbon data requirements into supplier contracts — a trend that will disproportionately benefit Fujian's larger, better-resourced enterprises over smaller competitors.

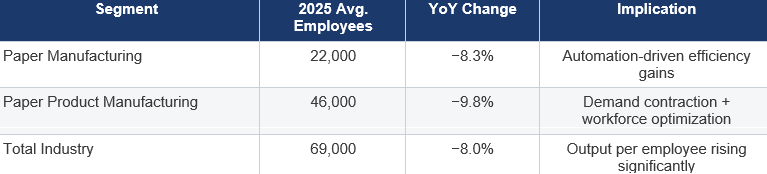

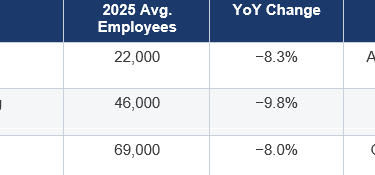

7. Workforce & Operational Efficiency

The paper industry's average workforce declined 8% year-on-year to 69,000 employees in 2025. Within this, paper manufacturing employment fell 8.3% (to 22,000) and paper product manufacturing fell 9.8% (to 46,000). This workforce reduction occurred against a backdrop of rising output — a strong indicator of productivity improvement and automation adoption across the sector.

The divergence between rising output and declining headcount reflects the capital intensity of modern paper manufacturing and the strategic priority placed on lean operations by Fujian's leading enterprises. Revenue per employee — approximately RMB 1.67 million at the industry level in 2025 — is a metric to watch as digital transformation accelerates further.

8. 2026 Outlook & Strategic Priorities

8.1 Macro Trajectory

In 2026, Fujian Province's paper industry is entering a critical period of high-quality development. The macro trends that will define performance include:

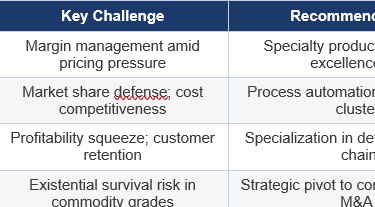

TREND 1: Slower Capacity Growth — After significant greenfield and brownfield capacity additions in 2024–2025, the pace of new capacity commissioning is expected to moderate in 2026. This should provide some relief to pricing pressure across packaging grades.

TREND 2: Structural Optimization — The industry will continue to consolidate around leading integrated enterprises, with small and medium-sized manufacturers in commodity grades facing the most acute pressure to differentiate or exit.

TREND 3: Green Manufacturing Deepening — Regulatory compliance requirements under China's Dual Carbon strategy and EPR framework will increasingly favor enterprises with established green credentials, creating both compliance costs and competitive differentiation opportunities.

TREND 4: Specialty Paper as a Profit Engine — Higher-margin specialty paper and functional pulp products will attract disproportionate R&D and capital investment, driven by demand from emerging sectors including new energy, electronics packaging, biodegradable food-service ware, and advanced medical applications.

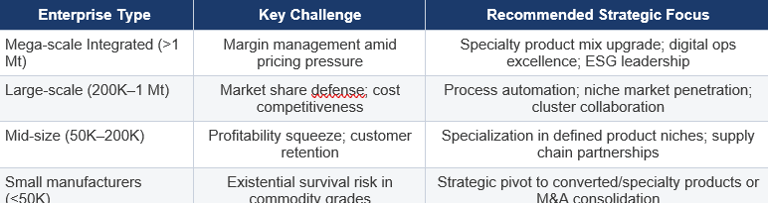

8.2 Strategic Priorities by Enterprise Type

8.3 Investment Considerations

• The paper packaging market is projected to grow at ~4.8% CAGR nationally through the late 2020s — above GDP growth — driven by e-commerce, plastic substitution, and food sector demand. Fujian's cluster structure positions it to capture above-average share of this growth.

• Pulp self-sufficiency is a structural advantage for integrated operators, reducing exposure to global softwood and hardwood pulp price volatility. Further integrated capacity investments by Zhangzhou-area enterprises are likely.

• Specialty paper development represents the highest-return capital deployment opportunity in the current cycle. Enterprises with proven specialty paper capabilities warrant premium valuations relative to commodity paper producers.

• Workforce optimization and digital transformation are reliably generating productivity improvements; enterprises with advanced automation programs should deliver ongoing margin improvement independent of paper price cycles.

• ESG / carbon credentials will increasingly determine export market access and procurement eligibility; enterprises investing early in carbon accounting and SBTi-aligned targets will avoid a compliance catch-up cost later.