When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

Global Paper & Packaging Sector —Weekly Earnings Review

PAPER INDUSTRY NEWS

Jino John

5/23/20263 min read

Executive Summary

Key Themes This Week

Indian paper demand appears to be stabilizing after multiple weak quarters.

Packaging and paperboards are outperforming commodity pulp businesses.

Margin recovery is uneven and still vulnerable to imported low-cost paper.

European and Japanese producers remain under pressure from energy, freight, and weak pulp cycles.

Companies with integrated forestry assets and diversified packaging exposure are proving more resilient.

Company-by-Company Analysis

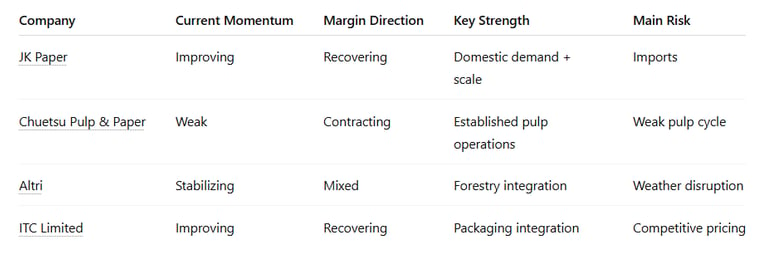

JK Paper

Financial Highlights

JK Paper reported a strong Q4 FY26 recovery supported by higher sales volumes and improved realizations. Consolidated turnover reached approximately ₹2,111 crore, while EBITDA improved to about ₹279 crore. Profitability rebounded sharply versus the weak FY25 base.

What Drove Performance

Record core paper volumes helped absorb fixed costs.

Copier and packaging board demand improved sequentially.

Better operating leverage supported EBITDA expansion.

Cost pressures moderated compared with earlier quarters.

Strategic Signals

Management appears focused on:

premium paper mix,

packaging board expansion,

and operational efficiency.

The company also maintained shareholder returns through a ₹4 dividend recommendation.

Risks

Imported paper from Asia remains a pricing threat.

Wood and pulp cost inflation could reappear quickly.

Industry capacity additions may pressure realizations in FY27.

Outlook

JK Paper looks positioned for cyclical recovery if domestic demand continues improving and imports remain manageable.

Chuetsu Pulp & Paper

Financial Highlights

Chuetsu Pulp & Paper reported lower FY2025 operating profit amid:

weak overseas pulp markets,

higher distribution costs,

and softer domestic demand conditions.

What Hurt Performance

Export pulp pricing remained weak.

Freight and logistics costs rose materially.

Domestic paper consumption in Japan stayed sluggish.

Currency and energy volatility pressured margins.

Strategic Signals

The results reinforce how vulnerable commodity pulp producers remain in the current cycle. The company’s exposure to global pulp pricing limited pricing power.

Risks

Continued weakness in Chinese pulp demand.

Global oversupply in commodity pulp markets.

Persistent energy inflation in Japan.

Outlook

Near-term recovery depends heavily on:

global pulp price normalization,

freight stabilization,

and Asian demand recovery.

Among the companies reviewed this week, Chuetsu appears the most operationally pressured.

Altri

Financial Highlights

Altri emphasized resilience despite severe weather disruptions affecting operations during the quarter. The company signaled expectations for gradual recovery as operational conditions normalize.

Key Takeaways

Climate-related operational disruptions are becoming financially material for pulp producers.

Despite temporary production impacts, management emphasized resilience and recovery capability.

Integrated forestry assets likely helped mitigate supply shocks.

Strategic Signals

Altri’s messaging focused on:

operational continuity,

sustainability,

and long-term recovery confidence.

This reflects a broader trend where ESG-linked resilience and forestry management are becoming strategic advantages.

Risks

Climate volatility and wildfire risk in Europe.

Continued pulp-market weakness.

Energy price instability.

Outlook

Altri may recover operationally faster than pure commodity peers because of:

vertical integration,

forestry access,

and disciplined balance-sheet management.

ITC Limited — Paperboards, Paper & Packaging Segment

Financial Highlights

ITC’s Paperboards, Paper & Packaging (PSPD) business delivered a strong sequential recovery in Q4 FY26 after prolonged weakness. The broader company also surprised positively on operating margins.

What Improved

Better packaging demand recovery.

Improved operating efficiencies.

Stabilization in input costs.

Stronger premium packaging demand.

Structural Strengths

ITC benefits from:

integrated pulp and packaging operations,

captive demand from FMCG businesses,

and leadership in sustainable packaging.

Its sustainable packaging investments continue gaining strategic importance.

Risks

Cheap imports still pressure domestic pricing.

Packaging demand remains tied to FMCG consumption trends.

Competition from regional players persists.

Outlook

ITC’s PSPD business may be entering an early-stage earnings recovery cycle, especially if:

FMCG demand strengthens,

premium packaging grows,

and sustainable alternatives gain market share.

Cross-Sector Trends Emerging This Week

Comparative Positioning

Investor Interpretation

Bullish Signals

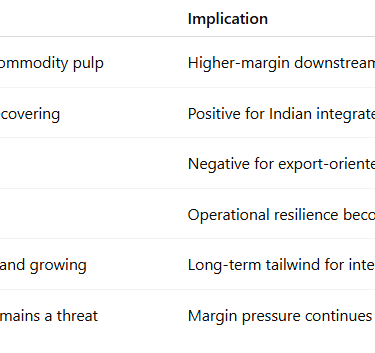

Indian paper cycle may have bottomed.

Packaging demand is healthier than commodity printing paper.

Integrated business models are outperforming standalone pulp producers.

Sustainable packaging remains a structural growth theme.

Bearish Signals

Commodity pulp markets remain weak globally.

Import pressure continues hurting pricing discipline.

Freight, energy, and climate risks remain elevated.

Recovery remains volume-led rather than pricing-led.

Sector View Going Forward

Most Resilient Business Models

Integrated packaging + paper companies

Forestry-backed pulp producers

Companies with captive demand ecosystems

Most Vulnerable

Commodity pulp exporters

Firms dependent on spot pulp pricing

Producers exposed heavily to imported paper competition

Overall Weekly Conclusion

This week’s earnings reinforce that the paper industry is splitting into two distinct groups:

Integrated packaging-led companies are beginning to recover with improving margins and stronger domestic demand.

Commodity pulp-heavy businesses remain trapped in a weak pricing environment with cost inflation pressures.