When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

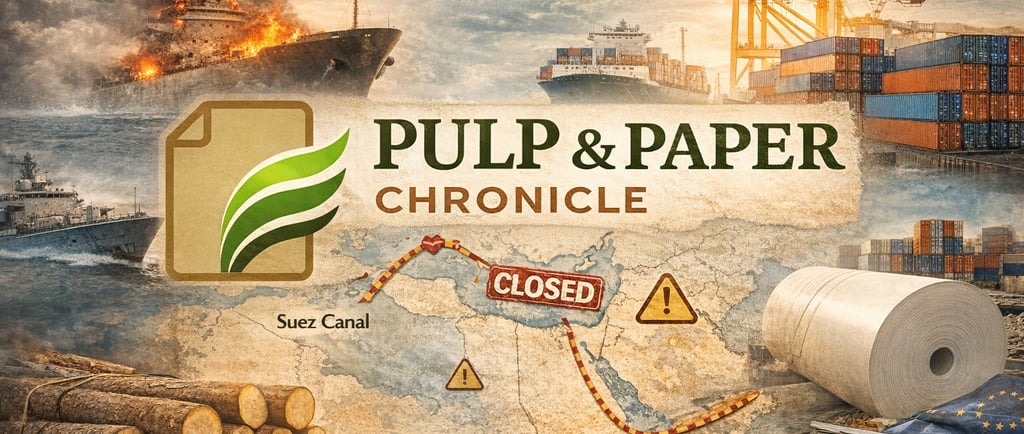

How the Middle East war is Reshaping Europe’s Paper Industry

MARKET ANALYSIS

Jino John

3/3/20263 min read

The renewed war in the Middle East is not just a regional shock — it’s a global logistics and cost event. For Europe’s pulp & paper sector, the consequences are immediate (longer voyages, rising freight and insurance costs), medium-term (margin pressure, production curtailments) and potentially structural (reshoring, accelerated decarbonisation investments). This piece pulls together shipping, insurance, energy and industry data to explain what’s happening now, what’s likely next, and what European producers, buyers and policymakers should do.

Why a war far away matters to Europe’s paper mills

Three transmission channels explain the link between Middle East fighting and Europe’s paper industry:

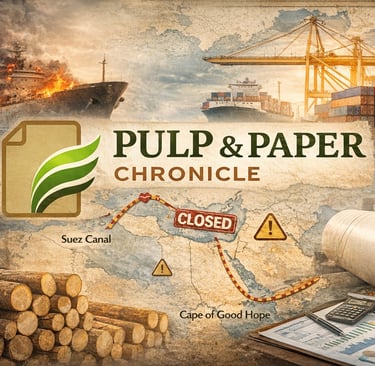

Maritime chokepoints and rerouting. The Strait of Hormuz and Suez Canal are key arteries for oil, LNG and container flows. Attacks and threats have led carriers to suspend or reroute services; many ships now sail around southern Africa, adding days–weeks to Asia–Europe round trips. That raises transit time, vessel utilisation and per-shipment cost.

War-risk insurance repricing. Major marine insurers have cancelled or heavily repriced Gulf war-risk cover; when insurers withdraw capacity or hike premiums, shipping lines and shippers either pay much more or avoid routes entirely — costs usually pass down to exporters and importers.

Energy price shock. The conflict has pushed oil and gas prices up; Europe is especially exposed given its energy linkages and recent tight gas markets. Paper and pulp are energy-intensive; higher energy prices hit mill operating costs, reducing margins or forcing temporary curtailments.

(These are the five most load-bearing facts behind the analysis: shipping reroutes/delays, insurer cancellations/pricing, oil/gas price spikes, Suez/Hormuz closures/threats, and the energy intensity of pulp & paper. )

What’s happening right now (short-term, days–weeks)

Transit times & costs spike. With Suez/Red Sea transits suspended or limited, Asia-Europe voyages detouring via the Cape add roughly 10–20+ days and materially higher bunker fuel and charter costs. That directly increases landed costs for pulp, rolls and paperboard shipped from European ports to Asia and for returning empties.

Insurance bills jump. Some insurers have cancelled war cover effective immediately, forcing short-term premium surges and gaps in coverage. Exporters face either higher freight surcharges or carriers refusing certain cargoes/routes.

Energy costs bite. Brent and regional gas prices jumped as shipping and tanker attacks reduced flows; mills that buy gas/fuel at spot markets see immediate margin erosion and potential curtailment pressure. Policy signals (EU, ECB) now also point to macro uncertainty that affects trade demand.

Medium term (3–12 months): who wins, who loses

Resilient: packaging & containerboard. Structural demand for packaging — driven by e-commerce and FMCG — keeps volumes relatively healthy. But margins will be compressed if freight/energy surcharges persist.

Vulnerable: graphic and speciality low-margin grades. Products already under demand pressure (newsprint, coated papers) are likeliest to see order cuts, rationalisation or permanent capacity closures if cost shocks persist.

Trade rebalancing & nearshoring. Prolonged disruption will accelerate buyers’ searches for closer suppliers, regional inventories and modal shifts (rail, short-sea) — an erosion risk for long-haul European export flows to Asia. CEPi stats show Asia accounted for ~22% of European exports in 2025 — that’s a sizeable exposure to any Asia route disruption.

Structural risks for Europe’s industry

Competitiveness versus low-cost producers. Extended higher energy and logistics costs can tilt competitiveness towards regions with cheaper energy or shorter trade distances to Asia. European mills already face pressure from overcapacity elsewhere.

Investment delays in decarbonisation or efficiency. Tight margins may force mills to postpone capital upgrades — but delaying energy-efficiency or electrification projects could be self-defeating given the energy exposure.

Supply chain fragility revealed. Chokepoint disruptions expose inventory and contract vulnerabilities — firms without hedges or alternate routes will be hit hardest. Studies estimate substantial economic loss from chokepoint disruption, underscoring systemic risk.

Practical, high-value actions for European players (operational & policy)

For mill managers, traders and policymakers — a prioritized playbook:

Immediate (days–weeks)

Map exposure: flag contracts and customers whose lanes transit Suez/Hormuz; quantify additional transit time and cost if rerouted.

Negotiate temporary war-risk/freight surcharges with customers and logistics partners; use transparent indexation where possible.

Secure short-term energy hedges and review forced-curtailment plans.

Near term (1–6 months)

Diversify logistics: explore short-sea, rail corridors (e.g., to/from Turkey/Black Sea/rail to China where viable), and alternative hubs for transshipment.

Prioritise high-margin SKUs for long-haul shipments; defer or regionalise low-margin cargoes.

Accelerate low-CAPEX energy efficiency measures (heat recovery, process optimisation).

Europe’s paper industry stands at a crossroads: the war’s immediate effect is logistical and cost pressure — but the real test will be whether firms and policymakers respond with short-term mitigation and medium-term resilience (energy hedging, logistics diversification, and targeted support). Failure to act risks shuttering marginal capacity and ceding market share to less-exposed regions; decisive action could instead accelerate efficiency and strengthen competitiveness.