When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

India–EU FTA Comprehensive report: Impact on India’s Paper & Pulp Industry

MARKET ANALYSIS

Jino John

1/27/20265 min read

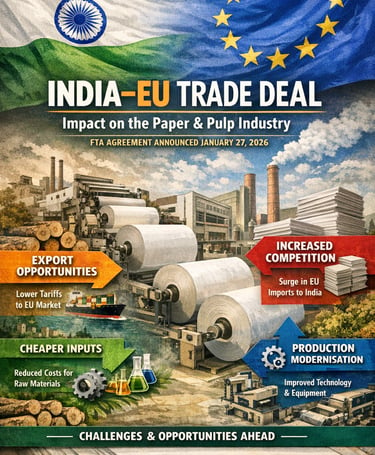

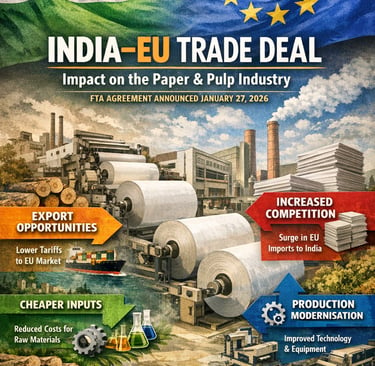

On 27 January 2026 India and the European Union announced a landmark Free Trade Agreement (FTA) that substantially reduces or eliminates tariffs on the vast majority of traded goods. The agreement is broad in scope and is expected to open market access in both directions over a phased implementation period.

This report assesses how the FTA is likely to affect the paper & pulp industry in India and in trade flows with the EU. Key takeaways for publication:

Net effect will be mixed. The FTA creates both opportunities (improved access for Indian exporters to the EU and lower-cost imported inputs) and challenges (heightened competition from EU producers entering India). The scale and timing of effects depend on the specific tariff line changes for paper, pulp and related inputs and the implementation timetable.

Paper is not singled out as a headline sector in initial media coverage; however, given the agreement’s very broad coverage of industrial goods, the majority of paper and paperboard tariff lines are likely to be affected under normal negotiating practice.

Immediate impact (2026–27) is likely modest. Many tariff cuts will be phased and require legal ratification; hence substantive trade shifts will be felt over several years after implementation.

Strategic opportunities exist. Indian manufacturers can expand exports of lower-value, labour‑intensive paper grades and packaging to the EU where tariffs fall; conversely, Indian demand for advanced coated and specialty papers may be met increasingly by EU suppliers unless Indian firms upgrade.

Policy actions can blunt downside risk. Targeted industry supports (technology upgrade incentives, carbon‑adjustment planning, and export promotion) will materially affect outcomes.

2. Scope, methodology and assumptions

This report synthesises public announcements of the India–EU FTA (Jan 27, 2026), recent trade press, and standard trade-impact frameworks to produce a publishable, practitioner‑oriented analysis. Where specific tariff schedules were not yet publicly released for individual HS lines, the report uses conservative assumptions and presents an explicit sensitivity framework so readers can update results once tariff schedules are published.

Key assumptions:

The FTA will remove or substantially reduce tariffs on a large fraction of industrial goods in a phased manner.

Sensitive agricultural products and select protected lines will be excluded or phased more slowly; paper is not expected to be among the most protected exceptions but exact treatment is yet to be confirmed.

Implementation and ratification will take 6–24 months for major tariff lines depending on parliamentary procedures and technical annexes.

3. Short summary of the India–EU agreement (Jan 27, 2026)

(High level) The agreement is comprehensive and covers goods, services, investment facilitation and regulatory cooperation. Public statements indicate tariff liberalisation for roughly 96–99% of goods by value, with phased implementation for certain sectors. Key beneficiaries called out in public briefings included autos, machinery, chemicals, pharmaceuticals, textiles and beverages; the deal also contains provisions to support decarbonisation efforts.

Implication for readers: The breadth of coverage implies most industrial tariff lines (including many paper & paperboard categories, pulp machinery and chemicals) will be covered by the deal’s tariff liberalisation schedule, but the precise tariff reductions for each HS six‑digit line must be verified against the official tariff annex once published.

4. Overview of the paper & pulp sector (India & EU)

India — snapshot

Structure: Mix of large integrated players and many medium/SME mills. Key output: packaging grades dominate (containerboard, kraft paper), writing & printing grades, tissue, and smaller volumes of specialty/coated papers.

Trade orientation: India exports packaging, lower-cost writing papers and specialty niche products; imports are concentrated in higher‑end coated papers, certain specialty grades, pulp and capital equipment.

Vulnerabilities: Energy costs, availability of fibre (both virgin and recovered), environmental regulation, and modernization needs.

EU — snapshot

Structure: Highly automated, capital‑intensive, and technologically advanced. Strong global presence in specialty, coated, and high‑quality graphic papers as well as packaging and pulp.

Trade orientation: Exports high‑value and technology‑intensive paper grades and capital equipment; imports lower volumes of commodity packaging from cost‑competitive regions.

5. How FTAs influence the paper industry — transmission channels

Tariff changes on finished paper products — alter relative prices and competitiveness across markets.

Tariff changes on inputs (pulp, chemicals, machinery) — change production costs and upgrade incentives.

Non‑tariff measures & regulatory alignment — harmonisation can reduce compliance costs and open procurement markets.

Scale and competition effects — greater market access for EU firms can increase import competition in India; Indian exporters can scale up in the EU where duties fall.

Investment flows — reduced trade frictions may encourage EU investment in Indian mills or joint ventures to serve both markets.

Environmental policy interactions — Carbon Border Adjustment Mechanism (CBAM) and sustainability clauses may influence competitiveness particularly for energy‑ and emissions‑intensive mills.

6. Detailed impact analysis (by segment)

6.1 Commodity packaging papers & board

Export opportunity: Lower EU tariffs could improve Indian competitiveness for lower‑cost containerboard and kraft grades where transport and quality allow. Gains likely concentrated on specific subgrades and large‑volume buyers.

Import risk: EU producers could target Indian end‑users for high‑quality packaging or specialty folding carton substrates. Price pressure may accelerate consolidation among domestic producers.

Recommendation: Producers should prioritise cost leadership, scale efficiency, and speed of delivery. Invest in productivity and customer service to defend domestic share.

6.2 Writing, printing & coated specialty papers

Export opportunity: Limited — Indian producers are less competitive in high‑end coated graphic papers; niche or value‑added products may find pockets of demand.

Import risk: High—EU manufacturers of coated and specialty papers may expand supplies to Indian converters and brand owners, competing with local capacity.

Recommendation: Focus on downstream integration (cut‑size, conversion), and pursue premium niches (sustainability labels, recycled content) to differentiate.

6.3 Pulp, chemical inputs, and capital equipment

Inputs: Tariff relief on pulp, bleaching chemicals, fillers and capital equipment lowers upgrade and production costs — a material positive for modernization.

Machinery & tech: Easier access to EU machinery and engineering services could speed upgrades, improve yield, and reduce emissions.

Recommendation: Use tariff relief to invest in energy efficiency, effluent controls, and automation. Seek concessional finance or public incentive programs to accelerate capex.

6.4 Recycled fibre and wastepaper flows

Policy harmonisation and tariff changes may shift economics of cross‑border wastepaper trade. If EU exports recovered fibre at lower effective cost, Indian recyclers could win, altering domestic collection economics. Attention to customs classifications will be needed.

7. Illustrative scenarios

Illustrative scenarios (fill with real numbers when tariff annex is published):

Conservative: Tariffs reduced by 50% over 5 years on paper lines — modest trade increase (5–10%) in affected segments.

Accelerated liberalisation: Tariffs fall to zero in 2 years — larger trade shifts (10–30%), import competition in specialty segments rises.

Input‑led upgrade: Tariff elimination on machinery and pulp lowers domestic costs, enabling 10–20% productivity gain over 5 years.

8. Risks and secondary effects

Timing & ratification risk: Changes won't be automatic; many tariff lines will be phased with legal ratification, moderating early shocks.

GSP and transitional rules: Changes to GSP or temporary withdrawal of preferences prior to FTA effect can create interim volatility.

Environmental regulation and CBAM: EU carbon rules could penalise high‑emission exports or favour mills with low‑carbon footprints.

Supply chain disruptions & currency fluctuations: Exchange rates and transport costs will mediate any price advantages.