When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

Pulp & Paper Chronicle – March 2026 Industry Update

MARKET ANALYSIS

Jino John

4/9/20263 min read

March 2026 confirms a 3-speed industry transformation:

🔵 Expansion Mode

Multi-billion-dollar projects (China, LATAM, India)

Packaging & tissue dominating investments

Strong push into bio-materials & specialty grades

🟠 Optimization Mode

Heavy restructuring, M&A, debt refinancing

Digitalization + automation across mills

Energy efficiency + decarbonization scaling

🔴 Pressure Mode

Global price increases

Weak pulp demand (Asia)

Shutdowns, safety risks, and geopolitical disruptions

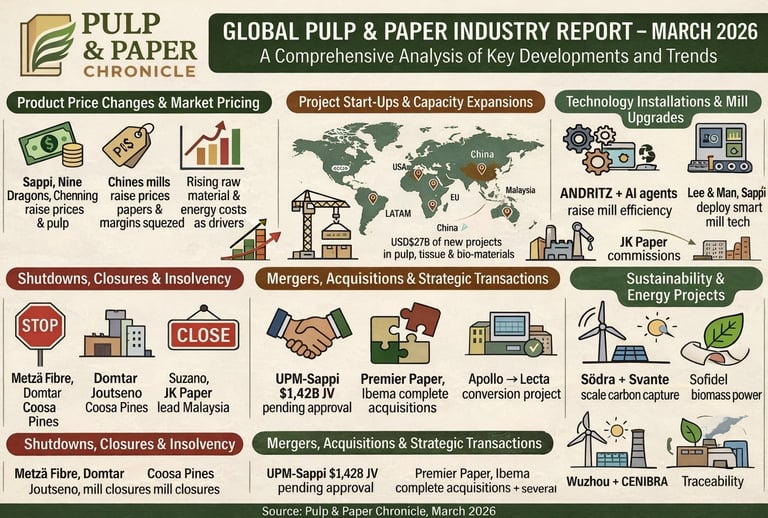

🤝 2. MERGERS, ACQUISITIONS & CONSOLIDATION

Major Completed Deals

Smurfit Westrock → Cartomanabí (LATAM expansion)

Premier Paper → PPB Ltd (UK)

SPB → Condat Mill (biopark transformation)

Imperial Dade + BradyPLUS merger

Ibema → BO Paper assets (Brazil)

OEM International → Weingrill (machinery entry)

Strategic / Ongoing Deals

UPM–Sappi €1.42B JV (pending approval)

Suzano–Kimberly-Clark JV under review

Reno de Medici debt restructuring (~€600M)

Global Sae-A selling paper division (~$1.4B)

Cartonpack → Agrypack

Nefab → Vallos

MIDLAND → Wetoska

Cascades + Solifor (fiber partnership)

👉 Trend: Platform building + vertical integration accelerating globally

💰 3. FINANCIALS, CAPITAL & FUNDING

Major Capital Investments

Lee & Man → RMB 27.5B integrated project

Jinguang → RMB 10.6B cellulose project

Wuzhou → RMB 5.44B + guarantees exposure RMB 8.77B

Sofidel → $775M US tissue plant

Suzano → $411M funding (BNDES)

Financial Performance Signals

Rayonier → weak demand, negative cash flow

SIG → dividend pause despite revenue growth

SCA → strong EBITDA margins (32%)

MEPCO → profitability recovery

👉 Trend:

Cash discipline + refinancing increasing

High leverage risk in expansion-heavy players

🏗️ 4. CAPACITY EXPANSION & MEGA PROJECTS

Asia (Dominant Growth Hub)

APP Rudong → 2M ton cellulose project

Century Sunshine → 2.65M ton integrated project

Nine Dragons → 650K ton + Phase IV expansion

APRIL → +150K tissue expansion

Wuzhou → +1M ton expansion

Americas

Sofidel → $775M tissue plant (USA)

Georgia-Pacific → $83M investment

Suzano → Ribas ecosystem development

Europe

Navigator → €115M tissue machine

Paracel → forestry-industrial hub

JK Paper → BCTMP commissioning

Paraibuna → Sapucaia expansion

Jingxing → Malaysia Phase II

👉 Trend:

Shift toward integrated mega-sites + regional supply hubs🚀 5. STARTUPS / COMMISSIONING / NEW FACILITIES

Toscotec (Greece) → 80K tpa tissue startup

Xuan Mai (Vietnam) → deinking pulp line

Valmet PM8 (China) → board line startup

Rengo (China) → packaging plant

SPG (USA) → new facility

Havix → hygiene/pet plant

👉 Southeast Asia emerging as recycled fiber growth hub

🔧 6. UPGRADES, MODERNIZATION & DIGITALIZATION

Key Upgrades

Ence → €11M digital + decarbonization upgrade

Guangdong Lee & Man → RMB 720M PM7 upgrade

Pavlovsky → press section upgrade

Palm → €20M modernization

Smart Mills & AI

Sappi → AI-driven MLOps

ANDRITZ + AI agents → 30% efficiency gain

Valmet → virtual sensors

Predictive maintenance adoption rising

👉 Trend: Transition to AI-enabled smart mills

🔄 7. REBUILDS, CONVERSIONS & STRATEGIC TRANSFORMATION

Norske Skog → packaging conversion strategy

SPB Condat → biopark + hydrogen hub

Fibre Excellence → restart + sale strategy

👉 Old graphic paper assets → packaging & energy hubs

🛑 8. SHUTDOWNS, RESTRUCTURING & CLOSURES

Major Shutdowns

Metsä Joutseno → demand-driven shutdown

Suzano → large-scale maintenance shutdown

APP Rizhao → 10-day shutdown

Closures / Restructuring

Smurfit Westrock → plant closure (USA)

Melitta → plant shutdown

Domtar → mill idling

Zhongshan Lianming → bankruptcy

Kyiv mill shutdown (geopolitical attack)

Fibre Excellence → raw material shortage

👉 Trend:

Capacity rationalization + demand correction (especially pulp)📦 9. PRODUCT INNOVATION & TECHNOLOGY

Packaging & Sustainability

MetsäBoard Pro FBB Go

Lecta PFAS-free papers

UPM SCK Forte

RubyPaper (inkjet photo paper)

Next-Gen Packaging

Fiber replacing plastic (DS Smith, PulPac)

Sitma automation → 50% speed increase

Paper-based cans (Sonoco + Pringles)

👉 Trend:

Fiber-based packaging replacing plastic at scale💲 10. PRICE INCREASES

🌍 Europe

Sappi Europe (Graphic Papers – UPDATED)

Mechanical coated reels: +€40/ton (March 2026)

Woodfree coated reels: +€50/ton (March 2026)

Woodfree coated sheets: ~€50/ton

Specialty papers: +€50–70/ton (effective April 2026)

👉 Driven by:

Rising energy, fiber, and logistics costs

Long-term price erosion in graphic paper segment

Strategic need to restore margins in declining market

👉 Strategic Signal:

Graphic paper pricing reaching unsustainable levels

Indicates:

Supply discipline

Potential capacity closures / consolidation

Reinforces structural decline of printing & writing paper

Other European Pricing Moves

Navigator → +4–7% (UWF papers)

SCA → +€100/ton (kraftliner)

Drewsen → price increase (April)

Solidus → increase effective April

🌏 Asia

Nine Dragons → multiple price hikes (3rd round in one month)

Shandong Chenming → +200 yuan/ton

Chinese specialty papers → +500 yuan/ton

General China market → +50–300 yuan/ton

🌎 Americas

Greif → +$60–70/ton (URB)

Sonoco → price increases (paperboard)

Koehler / Mitsubishi → specialty paper price increases

🌱 11. SUSTAINABILITY & ENERGY TRANSITION

Major Initiatives

UPM → heat recovery system

Sofidel → biomass boiler

Svante → carbon capture (500K tons CO₂)

Södra → renewable gas

CENIBRA → digital traceability

Circular Economy

Bamboo pulp (LC Paper)

EU packaging regulations

Recycling rates improving

👉 Shift:

From ESG commitments → industrial execution⚠️ 12. RISKS, INCIDENTS & EXTERNAL PRESSURES

Operational Risks

Fires (Sonoco, Woodland Pulp)

Gas leaks (Japan)

Fatal accidents (Asia Paper)

Structural Risks

Trade tensions

Logistics disruptions

Raw material shortages

Financial Risks

High debt exposure (Wuzhou, Reno de Medici)

🧭 FINAL STRATEGIC INSIGHT

🔥 WHAT DEFINES MARCH 2026

1. Industry is splitting:

📦 Packaging & tissue → growth engines

📉 Graphic paper → structural decline

2. Scale matters:

Mega investments in Asia

Consolidation in Europe & Americas

3. Technology is decisive:

AI, automation, smart mills

Energy optimization = competitive advantage

4. Sustainability = business model

Not optional anymore

Drives investment, innovation, and pricing

✅ FINAL VERDICT

March 2026 shows a fully transitioning industry:

Expansion (Asia-led)

Consolidation (global)

Optimization (efficiency + digital)

Pressure (costs + demand volatility)