When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

Pulp & Paper Chronicle’s Industry Update – April 2026

MARKET ANALYSIS

Jino John

5/7/20266 min read

Exclusive Monthly Industry Intelligence Report

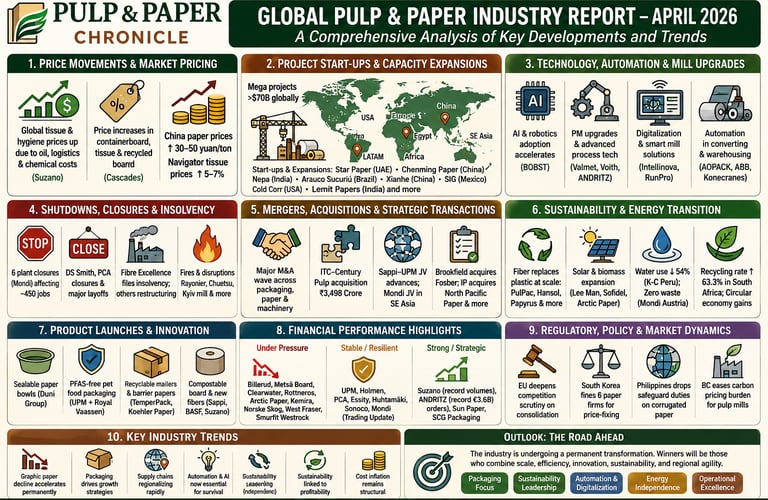

April 2026 marked one of the most transformational periods for the global pulp, paper, packaging, tissue, and converting industries in recent years. Across every region, the industry faced simultaneous structural pressure and strategic opportunity. The month was defined by aggressive consolidation, major capital investments, rising operational risk, accelerating sustainability mandates, and the rapid evolution of fiber-based packaging as a replacement for plastics.

🌍 MEGA THEMES DEFINING APRIL 2026

Structural decline in graphic paper accelerating

Traditional printing and writing paper segments continued contracting globally, forcing producers to restructure operations, reduce capacity, and redirect investments toward packaging and specialty grades.

Packaging dominates industry growth strategies

Corrugated packaging, recycled containerboard, paper bags, molded fiber, and food-service packaging remained the industry’s strongest growth engines.

Sustainability becomes a profitability driver

Sustainability is no longer treated as a compliance initiative. Companies are directly linking ESG execution with operational efficiency, cost savings, investor attractiveness, and long-term competitiveness.

Digitalization and AI reshape mill operations

AI-driven quality control, smart manufacturing, predictive maintenance, automation systems, digital printing, and integrated mill intelligence accelerated rapidly across the sector.

Cost inflation remains structural

Energy, logistics, chemicals, recovered paper, pulpwood, and labor inflation continued to pressure margins despite gradual volume recovery in several markets.

Consolidation wave intensifies

Acquisitions, joint ventures, recapitalizations, and strategic reviews accelerated globally as companies pursued scale, specialization, and geographic expansion.

🔴 1. GLOBAL FINANCIAL PERFORMANCE & EARNINGS SNAPSHOT

Margin pressure remained the central global story

Across the industry, volume recovery failed to fully offset escalating production costs and pricing volatility.

Companies facing profitability pressure

Billerud reported improved volumes but EBITDA margins collapsed to nearly 5%.

Metsä Board experienced a sharp decline in profitability amid weak European demand.

Clearwater Paper reported severe EBITDA deterioration.

Rottneros AB posted negative EBITDA and initiated a SEK 300 million rights issue for liquidity support.

Arctic Paper faced margin compression and falling sales.

Kemira, Norske Skog, and Segezha Group all reported weak quarterly results due to pricing pressure and market softness.

West Fraser recorded losses linked to duties and weak wood-product markets.

Companies maintaining resilience

UPM-Kymmene Corporation maintained relatively stable margins while energy operations supported profitability.

Holmen benefited from strong renewable energy contributions.

Packaging Corporation of America delivered relatively stable packaging-driven performance.

Essity maintained margins through pricing discipline and cost management.

Huhtamäki sustained operational stability despite inflationary conditions.

Sonoco improved profitability through pricing and cost optimization despite lower sales volumes.

Strong strategic performers

Suzano delivered record shipment volumes despite foreign exchange pressure.

ANDRITZ announced a record €3.6 billion order intake, highlighting sustained global capital investment momentum.

SCG Packaging posted profit growth supported by Indonesian market recovery.

Sun Paper achieved revenue and profit growth driven by capacity expansion and operational upgrades.

Key industry takeaway

The industry is transitioning into a structurally lower-margin environment where efficiency, scale, automation, and energy integration increasingly determine competitiveness.

🟠 2. MERGERS, ACQUISITIONS & STRATEGIC CONSOLIDATION

April saw one of the strongest consolidation waves in recent industry history.

Major acquisitions and strategic deals

Kadant acquired voestalpine BÖHLER Profil.

CCL Industries acquired ALT Technologies.

ITC announced acquisition of Century Pulp in a ₹3,498 crore consolidation deal.

Brookfield acquired Fosber Group, strengthening packaging machinery capabilities.

International Paper acquired North Pacific Paper Company.

Imperial Dade Canada acquired Enterprise Paper.

Dunapack Packaging acquired Stora Enso’s German corrugated operations.

Nefab Group acquired Vallos Packaging Solutions.

Cartonpack Group acquired Agrypack’s business unit in Italy.

The Royal Group acquired Chillicothe Packaging and Churmac Industries.

Joint ventures and strategic alliances

Sappi–UPM JV advanced European graphic paper consolidation plans pending regulatory approval.

Mondi formed a Southeast Asia paper bag expansion JV.

UPM + Felix Schoeller expanded fiber-based barrier packaging collaboration.

Amcor accelerated fiber-packaging partnerships.

Aristo + Stora Enso collaborated on dispersion barrier board technology.

Regulatory scrutiny intensifies

The European Commission initiated deeper competition investigations into major industry consolidation efforts.

South Korea launched lawsuits and price-fixing investigations involving packaging producers.

Industry implication

The industry is rapidly consolidating around integrated packaging ecosystems, technology specialization, and regional supply chain dominance.

🔴 3. CLOSURES, LAYOFFS & RESTRUCTURING WAVE

Structural downsizing accelerates

The decline of traditional paper segments triggered widespread restructuring activity.

Major closures and workforce reductions

Mondi announced six plant closures impacting approximately 450 jobs.

DS Smith closed the Launceston facility affecting 167 workers.

Manroland Sheetfed shutdown affected more than 660 employees.

Papresa entered liquidation proceedings.

Packaging Corporation of America closed its Richmond facility affecting 110 workers.

Valmet announced temporary layoffs impacting 2,400 employees.

Andhra Paper Limited faced strike-related disruptions.

Fibre Excellence filed for insolvency amid soaring wood and energy costs.

Operational disruptions

Kyiv Cardboard & Paper Mill halted operations after a drone attack.

Rayonier experienced a major fire at its Jesup mill.

Chuetsu Pulp & Paper restarted operations after fire-related disruption.

Georgia-Pacific and Suzano initiated major maintenance shutdowns.

Key takeaway

Capacity rationalization is becoming structural rather than cyclical, especially in graphic paper markets.

🟢 4. EXPANSION, CAPEX & MEGA PROJECTS

Despite profitability pressure, global investment activity remained exceptionally strong.

Mega industrial investments

Sinar Mas Jinguang Project in China advanced with a staggering $77.6 billion investment.

Arauco Sucuriú Project ($4.6 billion) moved ahead of schedule.

Xianhe Co. launched a 1.3 million tpa project.

Bohui Paper initiated five upgrade projects adding 1.15 million tonnes of capacity.

General Emballage partnered with ANDRITZ for Africa’s largest paper machine.

Regional expansion & logistics

Suzano expanded North American logistics and terminal infrastructure.

Arauco Brasil invested $400 million into Santos port logistics.

Grupo Corporativo Papelera expanded U.S. operations.

SIG doubled Mexico capacity.

Jieya invested $68 million into Egyptian operations.

Packaging & recycled fiber expansion

Star Paper Mill (UAE) launched recycled containerboard operations.

Lemit Papers expanded recycled fiber capacity with a 150 TPD deinking line.

Cold Corr launched the first U.S. cold corrugation facility.

Chenming Paper restarted full production with 5.8 million tons capacity.

Strategic trend

Investment is overwhelmingly concentrated in:

Packaging

Recycled fiber

Export logistics

Energy integration

Emerging markets

🟡 5. TECHNOLOGY, AUTOMATION & INDUSTRY 4.0

Technology investments accelerated globally as companies sought operational efficiency and lower costs.

Major automation and process upgrades

BOBST advanced AI-driven robotics systems.

AOPACK introduced integrated digital box-making systems enabling ultra-short-run corrugated production.

Flex Asepto Egypt deployed ABB automation technologies.

Konecranes modernized warehouse automation systems.

Runtech Systems improved dryer section efficiency.

Valmet continued extensive modernization partnerships globally.

Advanced paper machine developments

Zhejiang Forest United Paper launched the world’s first OptiDry Coat double-pass air drying system.

Voith successfully started up the first DuoCentri NipcoFlex press with center belt technology.

JK Paper commissioned a 400 ADMT/day BCTMP facility with Valmet technology.

Kuantum Papers upgraded PM2 systems including QCS and DCS automation.

Industry implication

Automation is no longer optional — it has become central to survival, quality optimization, labor reduction, and energy efficiency.

♻️ 6. SUSTAINABILITY, ENERGY & CIRCULAR ECONOMY

April confirmed sustainability as the defining long-term industry investment theme.

Fiber replacing plastic at scale

Hansol Paper launched Protego HS paper-based packaging.

PulPac accelerated dry molded fiber commercialization.

Papyrus Australia advanced banana-fiber packaging commercialization.

Indonesia accelerated shifts from plastic toward paper and glass packaging.

Tetra Pak and Sterilgarda introduced paper-based aseptic barriers.

ESG execution and renewable energy

Kimberly-Clark Peru reduced water use by 54%.

Lee Man Paper launched solar power projects.

Arctic Paper invested SEK 285 million into pellet production.

Sofidel expanded photovoltaic energy systems.

Burgo Group advanced renewable energy transition programs.

Domtar intensified emissions and water-risk mapping initiatives.

Recycling & circular economy

South Africa’s paper recycling rate rose to 63.3%.

Mondi Austria achieved one year of zero waste to landfill.

RDM Group accelerated recycled cartonboard adoption initiatives.

Industry takeaway

Sustainability investments are increasingly tied directly to:

Margin improvement

Regulatory compliance

Energy independence

Investor attractiveness

Customer retention

📦 7. PRODUCT LAUNCHES & MATERIAL INNOVATION

Sustainable packaging breakthroughs

Duni Group introduced sealable paper bowls using MAP technology.

BASF expanded ecovio® compostable materials.

Nippon Paper launched SHIELDPLUS® solutions.

Koehler Paper introduced recyclable barrier paper.

UPM + Royal Vaassen developed PFAS-free pet food packaging.

TemperPack launched recyclable mailers replacing corrugated boxes.

Specialty and high-performance paper innovations

Stora Enso introduced Trayforma Brown.

MM Board & Paper launched ALASKA® BRIGHT NEW.

Troitskaya Paper developed antibacterial parchment paper using silver-ion technology.

Lecta expanded thermal and metallized paper offerings.

Strategic implication

Innovation priorities are converging around:

Recyclability

Lightweighting

Barrier performance

Food-contact compliance

Cost reduction

🔵 8. PRICING, COST INFLATION & MARKET VOLATILITY

Global pricing pressure intensifies

Suzano announced $50/ton pulp price increases.

Navigator increased tissue prices by 5–7%.

Cascades implemented broad packaging price hikes.

China paper markets recorded coordinated price increases.

Corrugated producers globally passed through higher kraft paper and energy costs.

Regulatory interventions

South Korea’s FTC fined six paper companies for price-fixing and ordered rollbacks.

The Philippines removed safeguard duties on imported corrugated paper.

Industry takeaway

Pricing volatility remains one of the industry’s greatest risks, with costs increasingly becoming structurally embedded rather than temporary.

⚫ 9. INDUSTRY STRUCTURAL SHIFTS

Major long-term shifts accelerating globally

Graphic paper demand continues structural decline.

Packaging remains the industry’s dominant growth platform.

AI and digital printing are transforming publishing and converting.

Private-label tissue demand continues rising.

Supply chains are regionalizing rapidly due to geopolitical instability.

Biomass, pellets, and renewable energy are becoming integrated profit centers.

🔮 FINAL STRATEGIC OUTLOOK

April 2026 confirmed that the global pulp and paper industry has entered a permanent transformation era.

The industry is no longer operating within traditional cyclical dynamics. Instead, companies are navigating:

Structural cost resets

Accelerated sustainability mandates

Packaging-led growth

Automation-driven competitiveness

Consolidation-led market reshaping

Energy integration and resilience strategies

The winners of the next decade will likely be companies capable of combining:

Scale

Digital manufacturing

Circular economy integration

Renewable energy systems

High-performance fiber innovation

Regional supply chain agility

The industry’s future is increasingly clear:

Packaging, sustainability, automation, and energy integration are becoming the four pillars of long-term competitiveness.