When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

Thunder Bay Pulp & Paper Ends Newsprint Production — What It Means for the Market

MARKET ANALYSIS

Jino John

1/23/20262 min read

Thunder Bay Pulp & Paper has confirmed it will cease newsprint mill operations in the first quarter of 2026, directly affecting up to 150 employees as demand dynamics in the paper market continue to shift.

This is not an isolated operational decision — it is a strategic pivot driven by structural market changes in North American newsprint demand and broader pulp and paper economics. Below is a data-grounded analysis.

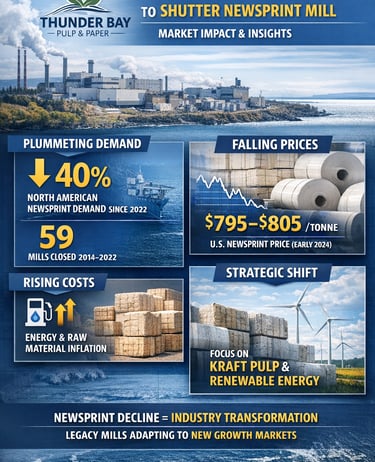

📉 Market Data: Newsprint Demand Has Plummeted

🔻 Sharp Decline in North American Newsprint Demand

Thunder Bay’s leadership cites a 40% decline in North American newsprint demand since 2022 as a core reason for the closure decision.

In 2025 alone, North American demand reportedly fell 18% year-over-year.

This drop reflects long-term structural shifts as advertisers and audiences increasingly move toward digital platforms — a trend that has eroded print volumes over the last decade.

📦 Industry Capacity Reductions

Over recent years, persistent demand erosion has led to massive capacity exits across North America. Industry sources estimate that at least 59 mills representing ~11.6 million tonnes of annual capacity have shut between 2014 and 2022 — many tied to newsprint and related grades.

📈 Cost & Price Pressures Compound the Challenge

📉 Falling Prices

Despite periodic spikes, newsprint prices have not rebounded to sustainable levels. For example, U.S. benchmark newsprint prices were reported near ~$795–$805/tonne in early 2024 — well below historical peaks and insufficient to offset fixed costs at many mills.

📈 Rising Input Costs

Energy, fibre, and freight costs remain significant for producers. Mills like Thunder Bay emphasize that input cost increases intensify the impact of lower volumes, since paper manufacturing has high capital and energy intensity that doesn’t scale down easily with declining output.

📌 Strategic Industry Implications

🧭 Trend: Structural Decline in Print

The evolution in newsprint mirrors decades-long global patterns where digital media competes with traditional print formats, steadily reducing demand for daily newspapers and directories — the core end-use for newsprint. Historical data going back years show dramatic declines in North American newsprint usage, often double-digit in annual contraction during earlier cycles.

💡 Pivot to More Stable Segments

While newsprint declines, other segments like kraft pulp for packaging and specialty paper grades remain more resilient due to stable or growing demand tied to e-commerce and sustainability trends. Thunder Bay has stated that it will continue operating its softwood kraft pulp line and renewable energy generation, possibly preserving jobs in those segments.

🌎 Broader Sector Shifts

This closure contributes to a wider pattern of mill curtailments in pulp and paper markets — not just newsprint — driven by a mix of aging assets, uneven demand, and cost pressures. 2025 saw multiple production changes across regions, underscoring shifting industry economics.

👥 Local & Workforce Impact

The planned shutdown affects about 150 onsite employees, with transitional support efforts underway with unions and government partners.

Importantly, the broader forest sector ecosystem around Thunder Bay supports thousands of jobs spanning harvesting, hauling, milling, and logistics — meaning the closure touches wider regional economic networks even as other operations remain active.

📍 Key Takeaways for Market Stakeholders

✅ Newsprint demand contraction is structural, not cyclical — digital migration is the dominant force.

✅ North American industry capacity has significantly reduced over the last decade.

✅ Price and cost pressures limit profit potential even when markets temporarily tighten.

✅ Resilience lies in pulp and specialty markets, not traditional newsprint.

✅ Regional economies need targeted support to manage transitions in legacy segments.

🔐 Final Thought

The Thunder Bay newsprint closure is a canary in the coal mine for traditional print grades. Savvy investors, operators, and policymakers should view this not as an outlier, but as part of a sustained rebalancing of paper markets toward growth areas like packaging, recycled fibres, and bio-based products.