When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

US Paper & Packaging Industry Report (2026 Outlook) By Pulp & Paper Chronicle

MARKET ANALYSIS

Jino John

3/19/20263 min read

Post-Cycle Reset: Margin Compression, Strategic Restructuring, and the Path to Recovery

Executive Summary

The US paper and packaging industry concluded 2025 in a cyclical downturn marked by margin compression, subdued demand, and significant strategic repositioning across major players. However, entering 2026, the sector is transitioning toward early-stage recovery, driven primarily by cost optimization, portfolio restructuring, and disciplined capital allocation rather than a strong rebound in end-market demand.

This analysis is based primarily on Q4 2025 earnings releases, with selected companies also reporting full-year FY2025 results alongside quarterly disclosures. As such, it reflects the most recent available financial performance rather than a complete set of standalone annual reports across all companies.

Key findings from Pulp & Paper Chronicle analysis:

Earnings declined across much of the packaging value chain, with companies such as Graphic Packaging and Weyerhaeuser reporting significant EBITDA contraction due to weaker volumes and pricing pressure.

Clear divergence in performance has emerged:

Best-in-class operators (e.g., Packaging Corporation of America) sustained superior margins

Transformation-driven players (e.g., International Paper) are positioned for recovery

Mid-scale players (e.g., Clearwater Paper) face structural margin pressure

Strategic restructuring is reshaping the competitive landscape, including:

International Paper’s planned corporate separation

Smurfit WestRock integration

Portfolio simplification across Sonoco and others

2026 outlook is cautiously positive, with expected EBITDA growth driven by:

Cost-out initiatives

Operational efficiency gains

Gradual normalization of volumes

Market Definition & Coverage

This report evaluates the United States paper and packaging industry, with focus on:

Core Segments

Containerboard and corrugated packaging

Consumer paperboard packaging

Tissue and hygiene products

Industrial paper packaging

Timberlands and wood products

Companies Covered

International Paper

Smurfit WestRock

Packaging Corporation of America

Graphic Packaging

Sonoco

Kimberly-Clark

Clearwater Paper

Weyerhaeuser

Industry Overview (2025)

The US paper and paperboard sector remains a mature, consolidated industry:

Estimated total demand: 70–75 million tonnes

Packaging grades: ~60–65% of demand

Structural trends:

Packaging: steady growth

Tissue: stable and resilient

Printing & writing: structural decline

2025 Operating Environment

Volumes: flat to slightly negative

Pricing: mildly negative across packaging grades

Margins: compressed across most producers

Company Performance Analysis

International Paper – Transformation and Recovery Catalyst

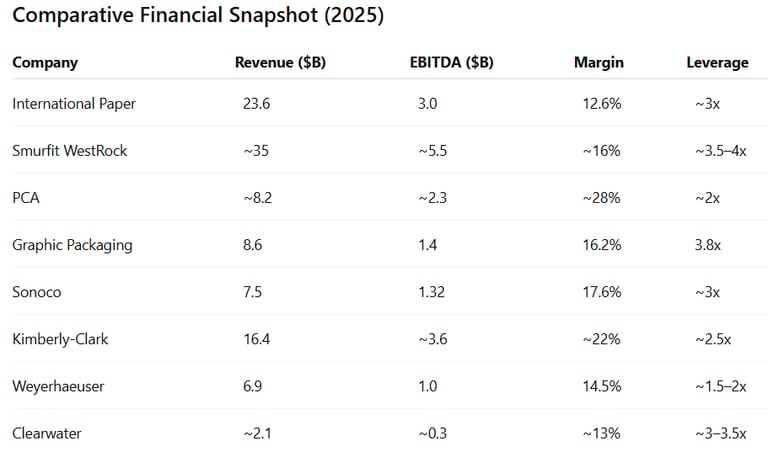

International Paper reported $23.6 billion in revenue and $3.0 billion in adjusted EBITDA in 2025, with reported losses driven by impairment and restructuring charges.

The company’s strategic shift toward two independent packaging businesses signals a major structural reset.

Pulp & Paper Chronicle View:

International Paper represents the strongest turnaround opportunity heading into 2026, supported by cost restructuring and portfolio focus.

Packaging Corporation of America – Operational Benchmark

PCA continues to demonstrate best-in-class execution, supported by:

Industry-leading EBITDA margins (~27–29%)

Strong vertical integration

Conservative leverage (~2x)

PCA sets the operational benchmark for North American containerboard producers.

Graphic Packaging – Margin Compression Under Pressure

Graphic Packaging reported:

Revenue: $8.6 billion (-2%)

EBITDA: down ~20% YoY

Margin decline from 19.1% to 16.2%

The company highlights the impact of weak pricing and cost inflation on mid-tier packaging players.

Sonoco – Growth Through Portfolio Expansion

Sonoco delivered strong top-line growth:

Revenue: $7.5 billion (+41.7%)

EBITDA: $1.32 billion (+27.9%)

Driven by acquisitions and productivity improvements.

Growth remains acquisition-led, with moderate organic momentum.

Kimberly-Clark – Defensive Margin Stability

Kimberly-Clark maintained:

Revenue: $16.4 billion

Organic growth: +1.7%

Strong margins supported by:

Brand strength

Productivity programs

Represents the most defensive earnings profile in the sector.

Clearwater Paper – Mid-Scale Structural Challenges

Clearwater operates in:

Bleached paperboard

Private label tissue

Facing:

Limited pricing power

Exposure to retail cost pressure

Mid-scale players remain structurally disadvantaged in the current cycle.

Weyerhaeuser – Cyclical Downturn Exposure

Weyerhaeuser reported:

Revenue: $6.9 billion

EBITDA decline from $1.3B to $1.0B

Driven by:

Weak housing demand

Lower lumber prices

Performance remains highly correlated to construction cycles.

Smurfit WestRock – Scale and Integration Strategy

Following its merger, Smurfit WestRock has emerged as the largest global packaging company, with focus on:

Synergies

Cost optimization

Portfolio integration

Execution of integration will determine long-term value creation.

Demand Drivers

E-commerce: long-term growth driver, short-term volatility

FMCG: stable but price-sensitive

Tissue & hygiene: resilient demand

Construction: key variable for wood products

Supply & Capacity Dynamics

Capacity rationalization (notably by IP)

Increased consolidation

Focus on:

Recycled fiber

Sustainable packaging

Higher-margin applications

Pricing & Cost Trends

Packaging prices declined modestly (~1%)

Fiber costs easing

Energy costs remain volatile

➡️ Net result: margin pressure in 2025

2026 Outlook

Base Case

Volume growth: +1–2%

Pricing: stable

EBITDA growth driven by cost savings

Upside Scenario

Strong demand rebound

Pricing recovery

Downside Scenario

Continued weak volumes

Persistent price pressure

Strategic Conclusions

2025 marked a cyclical trough for profitability

Recovery in 2026 will be gradual and cost-driven

Operational execution now outweighs scale advantages

Industry consolidation will continue to reshape competition

Pulp & Paper Chronicle – Strategic Takeaways

PCA remains the benchmark for operational excellence

International Paper offers the strongest turnaround potential

Kimberly-Clark provides defensive earnings stability

Mid-tier producers face ongoing structural margin pressure

Consolidation and restructuring will define the next cycle

Cost discipline will drive earnings recovery in 2026

The sector is entering early recovery—not full normalization

Prepared by:

Pulp & Paper Chronicle – Market Intelligence Division

March 2026