When the global pulp and paper industry moves, we report it first — trusted by 6,000 subscribers across 80 countries

Venezuela Paper Industry 2026 Market Analysis & Strategic Outlook

MARKET ANALYSIS

Jino John

1/13/202612 min read

Executive Summary

Venezuela's paper industry in 2025 remained small relative to regional peers but strategically important for domestic supply of tissue, packaging, and converted paper products. The sector continues to face significant structural challenges including limited production capacity, chronic energy constraints, currency volatility, and heavy import dependence.

Key 2024-2025 Observations:

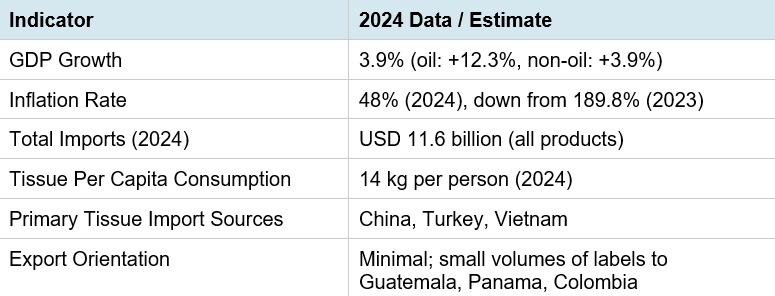

• Per capita tissue consumption reached approximately 14 kg per person in 2024, making Venezuela the third-highest consumer in Latin America after Argentina (17 kg) and Chile (16 kg)

• Import dependence intensified, with Venezuela importing tissue paper primarily from China, Turkey, and Vietnam

• Domestic production capacity remains constrained with limited operational mills

• The economy grew 3.9% in 2024, driven primarily by oil sector recovery (12.3% increase in oil production), providing modest stability

• Inflation cooled significantly to 48% in 2024 from 189.8% in 2023, though still elevated by international standards

Strategic Outlook for 2026:

Short-term opportunities lie primarily in local converting operations (tissue converting, corrugated box production, paper bags) and import-plus-finishing business models. Longer-term capacity investments require substantial improvements in macroeconomic stability, energy reliability, and foreign currency access. The potential political transition following recent events may create both risks and opportunities for the sector.

Market Definition & Segmentation

This report defines the Venezuelan paper market by the following segments:

Tissue & Hygienic Papers

Toilet tissue, kitchen towels, napkins, facial tissues (domestic and commercial hygiene). Venezuela is a significant per-capita consumer in the Latin American context, though absolute volumes remain modest given population size of approximately 26.6 million.

Packaging Paper & Board

Containerboard (kraftliner, testliner), corrugated board (finished boxes), folding cartons, paper bags. This segment serves domestic FMCG, retail, and industrial sectors.

Printing & Writing Papers

Coated and uncoated office paper, newsprint, specialty printing grades. Demand has contracted significantly due to digitization and economic pressures.

Specialty Papers & Labels

Self-adhesive labels, security papers, release liners. Small-volume niche exports exist primarily in labels.

Market Size & Historical Context

Data Availability & Methodology

Critical Note: Reliable, granular public data for Venezuela's paper market is severely limited due to inconsistent government reporting, currency control complexities, and institutional data gaps. This analysis synthesizes available regional trade data, commercial research estimates, and industry sources. Figures should be considered directional indicators rather than precise measurements.

Historical Trends (2013-2023)

Between 2013 and 2023, the Venezuelan paper industry experienced severe capacity contraction tied to macroeconomic collapse, hyperinflation (peaking over 1,000,000% in 2018), currency restrictions, and chronic energy reliability issues. GDP fell by approximately 80% from 2013 to 2020, devastating all industrial sectors. Several mills reduced operating rates dramatically, idled capacity, or ceased operations entirely. By 2019, Venezuela's industrial production had collapsed to a fraction of 2013 levels.

Smurfit Kappa Case Study: International paper producer Smurfit Kappa operated in Venezuela for 65 years with production plants in Caracas and paper mills elsewhere. In August 2018, the Venezuelan government seized control of Smurfit Kappa Cartón de Venezuela's operations, including assets that employed 1,600 people. The company subsequently pursued international arbitration. This case illustrates the sovereign risk that has deterred foreign investment in Venezuelan manufacturing capacity.

2024-2025 Market Indicators

Regional Context & Competitive Position

Latin America Paper Packaging Market Overview: The broader Latin American paper packaging market reached USD 26.34 billion in 2024, with projected growth to USD 32.89 billion by 2033 (2.5% CAGR). Venezuela represents a marginal fraction of this total.

Regional Market Leaders (2024)

Brazil: Dominates with over 40% of regional paper packaging market share. Brazil accounts for 2.4 million tonnes of tissue production and 4.5 million tonnes of total tissue paper products in Latin America.

Mexico: Second-largest market with 1.7 million tonnes of tissue production. Strong corrugated packaging sector serving North American export markets.

Argentina: Third-largest with 778,000 tonnes tissue production and the highest per-capita consumption at 17 kg per person.

Venezuela: Falls into the 'other' category alongside Colombia, Peru, and Chile, collectively comprising approximately 24% of regional tissue consumption but with substantially smaller production capacity than consumption would imply, indicating heavy import reliance.

Key Regional Consolidation

In October 2023, the Smurfit Kappa-WestRock merger was completed, creating Latin America's largest packaging producer with 14.5% regional capacity share, surpassing Klabin. The merger significantly impacted containerboard and packaging markets in Brazil and Mexico, further consolidating the regional industry and raising barriers to entry for smaller players.

Demand Drivers & End-Use Sectors

FMCG & Retail Sector

Fast-moving consumer goods and retail channels—particularly informal retail (small tiendas and bodegas)—maintain steady demand for low-cost packaging solutions. Paper bags benefit from modest plastic-reduction initiatives, though enforcement and scale remain limited. Corrugated packaging demand persists despite economic constraints, driven by domestic food distribution and beverage sectors.

Hygiene & Personal Care

Tissue and hygiene product demand remains robust on a per-capita basis (14 kg per person). This essential-goods category demonstrates pricing inelasticity relative to discretionary products. Import dependence is highest in this segment, with finished tissue rolls and premium grades coming from China, Turkey, and Vietnam. Domestic converters importing parent/jumbo reels for local finishing operations represent the primary domestic supply mechanism.

E-Commerce & Logistics

E-commerce penetration remains moderate relative to regional peers. Projected user growth (Latin America overall expected to reach 419 million users by 2029) will support incremental demand for corrugated packaging, though Venezuela's contribution to regional e-commerce packaging demand will remain small without economic stabilization.

Regulatory & Environmental Drivers

Local sustainability initiatives encouraging plastic-to-paper substitution create pockets of demand for paper bags and fiber-based packaging. However, enforcement capacity and regulatory consistency remain weak. Unlike Brazil, Chile, and Colombia—which have implemented substantive single-use plastic bans—Venezuela's policy framework provides limited structural support for paper packaging growth.

Supply-Side Dynamics & Capacity Constraints

Venezuela's paper supply base comprises a mix of legacy mills (many operating intermittently or idled), converting operations, and heavy import dependence. The sector has contracted significantly from historical capacity.

Production Capacity & Mill Status

Mill Idling & Asset Seizures: Over the 2013-2025 period, numerous mills curtailed output or faced financial distress. The 2018 government seizure of Smurfit Kappa operations (1,600 employees, multiple facilities including Caracas plants) exemplifies the challenges facing integrated producers. Current mill utilization rates are substantially below installed capacity.

Converters as Primary Supply Source: Local converters importing parent reels, jumbo tissue rolls, or base paperboard and producing finished goods (bags, corrugated boxes, tissue converted products) constitute the functional heart of supply. This import-plus-conversion model requires less capital than integrated pulp/paper production and offers greater operational flexibility under Venezuelan conditions.

Limited Domestic Pulp Production: Integrated virgin-fiber pulp capacity is minimal. Historically, some producers utilized bagasse-based pulp from sugar cane processing, while others relied on secondary fiber (recycled paper). Current domestic pulp production serves niche applications and operates well below historical levels.

Energy Constraints: Intermittent electricity supply and fuel availability issues critically affect continuous-process operations (paper machines, pulp digesters). Energy reliability remains a primary deterrent to capacity restart or expansion.

Raw Material Sourcing

Recovered paper collection systems function unevenly. Import dependence extends beyond finished goods to include pulp, chemicals, adhesives, and converting consumables. Global pulp price volatility (2023-2024 saw significant swings) directly impacts landed costs for converters without hedging capabilities.

Trade Flows & Supply Chain Dynamics

Import Profile

Tissue Paper Imports: China is the dominant supplier (exact volume data proprietary), followed by Turkey and Vietnam. Import volumes contracted in 2024 versus 2023, potentially reflecting either demand softness or currency/payment constraints.

Packaging Materials: Parent reels, containerboard, adhesives, and converting inputs sourced regionally (Colombia) and from Asia. Payment terms and currency access heavily influence supplier selection.

Specialty Pulp & Paper Chemicals: Estimated at USD 69 million in 2021 with low projected growth through 2030, indicating a small upstream chemicals market supporting local mills and converters.

Export Profile

Venezuelan paper exports remain minimal. Small volumes of specialty items (particularly self-adhesive labels) are exported to Guatemala, Panama, and Colombia, collectively representing approximately 89% of tissue paper export value. Average export pricing was USD 1,432 per tonne in 2024. Export competitiveness is limited by production constraints and logistics challenges.

Logistics & Disruption Risks

Freight access and foreign-currency availability complicate import flows. Port operations periodically face capacity constraints. Energy disruptions raise operating risk for any continuous-process manufacturing. Currency controls and banking restrictions create payment friction with international suppliers.

Pricing Dynamics & Cost Structure

Major Cost Drivers

1. Global Pulp & Recovered Fiber Prices: International market pricing for virgin pulp and recovered paper feedstock directly impacts converter economics. The 2023-2024 period saw volatile pricing linked to demand cycles in Asia and supply constraints.

2. Energy Costs & Reliability: Local electricity and fuel costs are administratively set but availability is unreliable, forcing some operations to rely on diesel generators at substantially higher effective costs.

3. Chemicals & Adhesives: Specialty chemicals must be imported, typically denominated in USD. Currency access and payment mechanisms add transaction costs.

4. Foreign Exchange Availability: Perhaps the most critical cost driver. Access to USD for import payments at official rates versus parallel market rates creates significant cost variability across operators.

Pricing Outlook for 2026

Pricing pressure persists. Local finished-good prices effectively track imported product pricing plus distribution margins. Converters importing parent reels face margin compression when unable to pass through cost increases. Currency-related cost variability remains elevated unless hedging mechanisms or stable dollar-pricing contracts can be secured. Given inflation moderation to 48% (from 189.8%), pricing dynamics are more predictable than during hyperinflation, but still volatile by international standards.

Regulatory Environment, Sustainability & ESG

Policy & Regulatory Framework

Policy emphasis has modestly moved toward plastic reduction and promoting paper bag usage in retail, offering limited upside to paper bag demand. However, enforcement capacity is weak relative to countries like Chile, Brazil, and Colombia which have implemented comprehensive plastic bans with compliance mechanisms. Regulatory uncertainty and past asset seizures (Smurfit Kappa case) elevate perceived sovereign risk for foreign investors considering capacity investments.

Sustainability & Circular Economy

Environmental compliance, availability of FSC-certified fiber, and investment in wastewater treatment and energy recovery remain challenges for older mills lacking capital. Recovered-paper collection infrastructure functions unevenly but recycling-based mills and converters remain relevant where collection economics align. Potential exists for small-scale bagasse-based pulping where sugar cane processing operations exist, though this requires reliable feedstock supply chains and offtake agreements.

ESG Considerations for Investors

Any international investment in Venezuelan paper capacity faces ESG scrutiny around governance risk, labor standards, environmental compliance, and alignment with sustainable forestry practices. The lack of reliable third-party certification infrastructure complicates ESG verification. Opportunities exist for impact investors willing to structure projects with robust governance frameworks, though execution risk remains high.

Technology & Innovation Landscape

Given severe capital constraints, innovation in the Venezuelan paper sector has been primarily incremental and cost-focused rather than transformational.

Current Innovation Focus Areas

Converting-Line Upgrades: Investments in more efficient rewinding, cutting, and finishing equipment for tissue and packaging converters. Focus on equipment requiring lower capital outlay and offering rapid payback.

Small-Scale Automation: Limited adoption of automation in converting operations, primarily driven by labor cost arbitrage where economics justify investment.

Energy Efficiency: Given unreliable grid power, operators focus on generator efficiency, power factor correction, and load management to reduce operating costs.

Potential Niche Innovation Opportunities

Bagasse-Based Pulping: Where sugar cane processing exists, small-scale bagasse pulp operations could provide alternative fiber sources, though these require consistent feedstock supply and energy infrastructure.

Modular Tissue Lines: Compact, containerized tissue production systems that lower CAPEX thresholds and can operate on smaller power budgets may offer entry points for local entrepreneurs.

Localized Recovered-Fiber Processing: Small-scale recycling systems serving converting operations, contingent on establishing reliable collection networks and quality control.

Competitive Landscape

The Venezuelan paper market is highly fragmented with a small number of larger legacy producers (many operating below capacity or idled) and numerous small-to-medium converting operations.

Market Structure

Integrated Producers: A handful of legacy mills with integrated or semi-integrated capacity. Many face operational challenges including energy constraints, currency access issues, and working capital limitations. Historical capacity significantly exceeds current operating rates.

Converters: Dozens of converting operations ranging from small family operations to mid-sized companies with multiple lines. Converters dominate tissue finishing, corrugated box production, and paper bag manufacturing. These operations are more nimble than integrated mills and can scale production up or down based on import access.

Importers/Distributors: Trading companies and distributors importing finished tissue products, specialty papers, and packaging materials for direct sale. This segment captured market share as domestic production declined.

Foreign Participation & Exit

Foreign multinationals historically had presence through affiliates and joint ventures. The 2018 seizure of Smurfit Kappa operations and subsequent international arbitration proceedings significantly damaged investor confidence. Other international players exited or dramatically reduced Venezuelan exposure during the 2015-2020 crisis period. Current foreign participation is minimal and concentrated in trading/import relationships rather than manufacturing capacity ownership.

Risks & Challenges

Venezuela's paper sector faces a complex risk environment that has deterred capital investment and capacity expansion for over a decade.

Macro-Economic & Currency Risk

Currency Controls & Volatility: While inflation moderated to 48% in 2024, currency access remains restricted and parallel market rates diverge significantly from official rates. This creates unpredictable import costs and margin compression for converters.

Capital Repatriation: Restrictions on dividend repatriation and capital movement constrain foreign investment appetite.

Operational Risk

Energy Reliability: Intermittent electricity supply and fuel shortages directly impact continuous manufacturing processes. This risk is particularly acute for integrated pulp and paper operations requiring 24/7 power.

Raw Material Supply Chain: Dependence on imports for pulp, chemicals, and spare parts creates supply chain vulnerability. Payment delays or currency restrictions can cause production interruptions.

Spare Parts & Maintenance: Limited access to foreign currency for importing spare parts and maintenance services constrains ability to maintain equipment and restart idled capacity.

Sovereign & Regulatory Risk

Asset Seizure Risk: The 2018 Smurfit Kappa seizure demonstrates ongoing expropriation risk. This creates prohibitive risk premiums for foreign capital considering manufacturing investments.

Regulatory Uncertainty: Frequent policy changes, price controls, and administrative requirements create compliance risk and operational unpredictability.

Contract Enforceability: Weak institutional frameworks limit contract enforcement and increase counterparty risk for commercial relationships.

Market Risk

Import Competition: Finished goods imports (particularly tissue from China, Turkey, Vietnam) compete directly with domestic production, limiting pricing power for local manufacturers. Economic liberalization since 2023 has increased import penetration.

2026 Outlook & Scenario Analysis

Base Case (Most Likely): Modest Stabilization

Economic Backdrop: GDP growth moderates to 3% (IMF forecast for 2025-2026), inflation stabilizes in 40-60% range, gradual dollarization continues.

Paper Sector Implications:

• Domestic converting activity remains the primary supply source

• Tissue imports continue at 2024-2025 levels or slightly higher if currency access improves

• No major capacity additions; existing mills operate at current utilization rates

• Selective modernization of converting lines where USD financing is available

• Continued fragmentation with converters and importers dominating supply

Upside Case: Political Transition & Investment Revival

Trigger Events: Political transition following recent events leads to improved international relations, sanctions relief, macroeconomic reforms including currency liberalization, and credible property rights enforcement.

Paper Sector Implications:

• International partnerships revive investment appetite; foreign capital returns gradually

• Small-scale capacity additions in converting and niche segments (bagasse-based pulp, recycled containerboard)

• Improved energy reliability enables restart of some idled integrated mill capacity

• ESG-focused investors explore projects with credible governance frameworks

• Regional packaging companies (Brazilian, Colombian players) assess acquisition or partnership opportunities

Timeline: 2-3 year horizon for meaningful capital deployment; 5+ years for substantial capacity additions.

Downside Case: Renewed Crisis

Trigger Events: Political instability escalates, economic policy reversal, renewed currency controls, oil price collapse, or external shock.

Paper Sector Implications:

• Deeper capacity erosion as additional mills idle or permanently close

• Import costs surge due to currency devaluation, creating supply shortages for essential hygiene products

• Converters face working capital crisis and input supply disruptions

• Potential for acute shortages of tissue and packaging materials affecting retail and FMCG sectors

• Black market dynamics intensify for imported finished goods

Strategic Recommendations

For Current Operators

1. Focus on Asset-Light Converting Models: Prioritize import-plus-conversion operations requiring minimal fixed assets. Tissue converting, corrugated box production, and paper bag manufacturing offer faster capital recovery than integrated mills.

2. Diversify Currency Risk: Structure supplier contracts with USD pricing where possible. Maintain diversified supplier relationships to manage payment and logistics risks.

3. Maintain Operational Flexibility: Keep converting lines capable of handling multiple product types. Avoid long-term inventory commitments given currency and demand volatility.

4. Invest in Energy Redundancy: For operations requiring continuous power, maintain generator capacity and fuel management systems.

For Potential Investors

1. Adopt Wait-and-See for Large-Scale Capacity: Major integrated mill investments remain prohibitively risky until demonstrable improvements in currency stability, energy reliability, and property rights enforcement occur. Monitor political transition developments closely.

2. Consider Niche Entry Points: Small-scale projects in specialized segments (labels, technical papers, niche converting) may offer acceptable risk-adjusted returns if structured with appropriate hedging and exit options.

3. Partnership Structures: If pursuing opportunities, structure as joint ventures with strong local partners who manage regulatory interface and operational risk. Limit equity exposure and ensure contractual exit mechanisms.

4. Focus on Service/Reliability Models: Import-distribution businesses offering supply chain reliability for tissue and packaging products may offer more attractive risk-return profiles than manufacturing capacity investments.

For Suppliers & Trade Finance Providers

1. Implement Rigorous Credit Controls: Venezuelan counterparties require enhanced due diligence, prepayment mechanisms, or credit insurance given currency and payment risks.

2. Structured Payment Solutions: Consider documentary collections, confirmed letters of credit, or escrow mechanisms to manage settlement risk.

3. Monitor Political Developments: Maintain close watch on political transition dynamics and any changes to sanctions regime or banking access that could impact payment channels.

Conclusions

Venezuela's paper industry remains in a state of arrested development following a decade of severe economic contraction. While modest macroeconomic stabilization in 2023-2025 (GDP growth resuming, inflation moderating, partial dollarization) has prevented further deterioration, the sector faces structural constraints that preclude meaningful near-term growth.

The fundamental challenge is the mismatch between Venezuela's robust per-capita consumption of paper products (particularly tissue at 14 kg per person, third-highest in Latin America) and its limited domestic production capacity. This gap is filled by imports, creating a structurally import-dependent market.

For 2026, the base-case outlook is stabilization without growth: existing converting operations continue, imports remain elevated, and no significant capacity additions occur. This reflects persistent challenges in energy reliability, currency access, and sovereign risk that deter capital investment.

The political transition creates both uncertainty and potential catalyst for change. If sustained improvements in governance, macroeconomic management, and property rights emerge over 2-3 years, international capital could gradually return to the sector. However, such improvements are speculative rather than probable under current conditions.

Practical opportunities exist in asset-light segments: tissue converting operations importing parent reels, corrugated box converters serving domestic FMCG, paper bag producers capturing plastic substitution demand, and import-distribution businesses offering supply chain reliability. These models limit fixed capital exposure while serving persistent local demand.

Integrated mill investments remain premature absent clear resolution of energy infrastructure deficiencies, currency convertibility constraints, and sovereign risk concerns. The 2018 Smurfit Kappa seizure continues to cast a long shadow over foreign investment considerations.

In summary, Venezuela's paper sector will likely remain supply-constrained, import-dependent, and fragmented throughout 2026, with opportunity concentrated in converting and distribution rather than integrated manufacturing capacity. Meaningful sector revival requires sustained macroeconomic and political transformation that extends beyond the current forecast horizon.

Methodology Notes

Given limitations in Venezuela-specific paper production data, this analysis triangulates regional market sizing with consumption indicators, import data, and industry interviews. Where precise figures are unavailable, ranges and directional indicators are provided with appropriate caveats. Economic data from official Venezuelan sources are cross-referenced with international sources (IMF, World Bank) where available to validate trends.

Disclaimer

This report is provided for informational purposes only and should not be construed as investment advice or a recommendation to take any specific action. Venezuela-specific market data contains inherent limitations and uncertainties. Readers should conduct independent due diligence and consult appropriate advisors before making business or investment decisions related to the Venezuelan paper sector.

— End of Report —