When the global pulp and paper industry moves, we report it first — trusted by 8,000 subscribers across 80 countries

China Paper and Paperboard Industry Production Report January–March 2026

MARKET ANALYSIS

Jino John

6/18/20263 min read

Overview

According to data released by the National Bureau of Statistics of China, China’s machine-made paper and paperboard industry maintained stable growth in the first quarter of 2026. From January to March 2026, the total output of machine-made paper and paperboard (excluding processing of purchased raw paper) by large-scale enterprises nationwide reached 40.188 million tons, representing a year-on-year increase of 5.1%.

The data reflects continued recovery in industrial demand, expanding packaging consumption, and stable growth in downstream sectors such as e-commerce, logistics, food packaging, and consumer goods manufacturing.

National Production Performance

China’s paper and paperboard production remained highly concentrated in coastal and manufacturing-intensive provinces. Eastern and southern provinces continued to dominate national output due to advantages in industrial clusters, export-oriented manufacturing, transportation infrastructure, and access to raw materials.

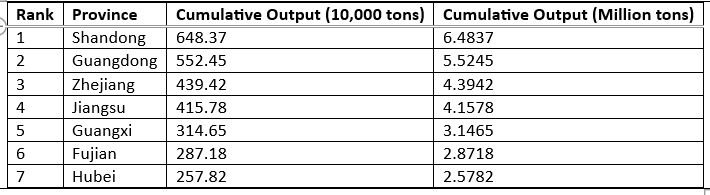

Top Producing Provinces (January–March 2026)

Together, the top four provinces accounted for more than half of national production, highlighting the strong regional concentration of China’s paper manufacturing industry.

Regional Analysis

1. Shandong Province Leads the Nation

Shandong Province ranked first nationwide with a cumulative output of 6.4837 million tons during the first quarter of 2026.

Key advantages supporting Shandong’s leadership include:

Strong industrial foundation in papermaking

Large-scale integrated paper enterprises

Well-developed logistics and port infrastructure

High concentration of packaging and export manufacturing industries

Stable domestic and overseas demand

Shandong has long been one of China’s core papermaking bases, particularly in packaging paper, containerboard, and industrial paper products.

2. Guangdong Maintains Strong Production Capacity

Guangdong Province ranked second with 5.5245 million tons of output.

As China’s largest manufacturing and export province, Guangdong benefits from:

Massive packaging demand from export industries

Strong e-commerce and consumer goods sectors

Advanced supply chains

High concentration of downstream converting enterprises

The province remains a major driver of packaging paper consumption and production growth.

3. Zhejiang and Jiangsu Form the Yangtze River Delta Production Hub

Zhejiang and Jiangsu together produced over 8.55 million tons during the quarter.

The Yangtze River Delta region continues to serve as one of China’s most advanced paper manufacturing clusters due to:

High industrial efficiency

Strong environmental compliance capabilities

Mature recycling systems

Advanced papermaking technologies

These provinces are particularly competitive in high-grade packaging paper and specialty paper production.

4. Guangxi Emerges as a Key Southern Production Base

Guangxi Zhuang Autonomous Region produced 3.1465 million tons, ranking fifth nationally.

The region has become increasingly important because of:

Rich forestry and pulp resources

Lower operating costs

Expansion of integrated pulp-and-paper projects

Policy support for industrial development

Guangxi is gradually strengthening its role in China’s pulp supply chain and integrated papermaking capacity.

Industry Trends

Stable Growth in Packaging Demand

The 5.1% year-on-year increase indicates resilient demand from:

E-commerce packaging

Food and beverage packaging

Consumer goods

Logistics and transportation industries

Containerboard and corrugated paper remain major growth drivers.

Continued Industry Concentration

Production remains concentrated among large-scale enterprises and developed industrial regions. Smaller producers continue facing pressure from:

Environmental compliance costs

Energy efficiency requirements

Raw material price volatility

Industry consolidation

Leading enterprises are expected to further increase market share.

Green and Sustainable Development

China’s paper industry continues transitioning toward:

Energy-efficient production

Low-carbon manufacturing

Recycled fiber utilization

Cleaner pulping technologies

Environmental regulations are accelerating modernization across the sector.

Outlook for 2026

Looking ahead, China’s paper and paperboard industry is expected to maintain moderate growth throughout 2026, supported by:

Stable domestic consumption

Recovery in industrial production

Expansion of e-commerce logistics

Ongoing urban consumption upgrades

However, the industry may still face challenges including:

Fluctuating pulp prices

International trade uncertainties

Environmental policy tightening

Energy cost pressures

Large integrated producers with strong supply chains and technological advantages are likely to continue outperforming the broader market.

Conclusion

China’s machine-made paper and paperboard industry achieved solid growth in the first quarter of 2026, with total national output reaching 40.188 million tons, up 5.1% year-on-year. Shandong Province maintained its leading position with output exceeding 6.48 million tons, followed by Guangdong, Zhejiang, and Jiangsu.

The data demonstrates continued resilience in China’s manufacturing and packaging sectors, while also highlighting the increasing concentration, modernization, and sustainability transformation of the country’s paper industry.