When the global pulp and paper industry moves, we report it first — trusted by 8,000 subscribers across 80 countries

Top 10 U.S. Paper Companies: Financial and Strategic Analysis of Q1 2026 Performance

MARKET ANALYSIS

Jino John

6/13/20262 min read

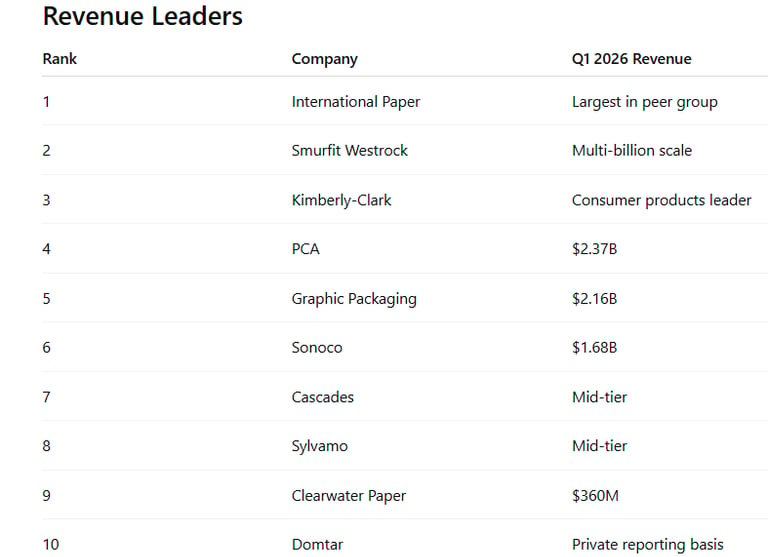

Q1 2026 Performance Analysis of 10 Leading North American Paper Companies

Companies Covered

Kimberly-Clark

International Paper

Smurfit Westrock

Packaging Corporation of America (PCA)

Graphic Packaging Holding Company

Cascades

Sonoco

Sylvamo

Clearwater Paper

Domtar

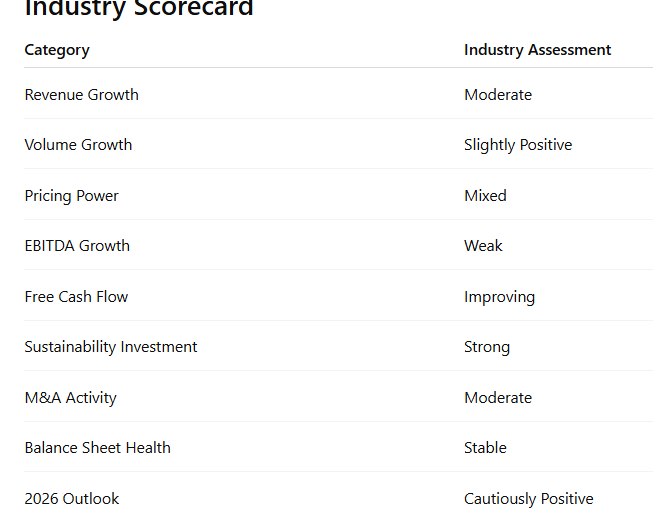

Executive Summary

The first quarter of 2026 revealed a paper and packaging industry operating in two very different environments.

On one side, packaging-focused companies continued to benefit from e-commerce demand, food packaging growth, plastic replacement initiatives, and pricing discipline. On the other, paperboard and commodity paper producers faced persistent pricing pressure, inflationary cost headwinds, and uneven industrial demand.

Three dominant themes emerged:

1. Cost Control Has Become the Primary Growth Strategy

Almost every company emphasized:

Workforce optimization

Facility rationalization

Supply-chain efficiency

AI-enabled procurement

Inventory reduction

Unlike previous years where volume growth drove earnings expansion, 2026 is increasingly becoming a margin-management story.

2. Sustainability Has Shifted From Compliance to Revenue Driver

Companies are no longer discussing sustainability solely as an ESG initiative.

Instead, they are monetizing:

Plastic-to-paper conversion

Recyclable packaging

Renewable energy investments

Circular economy solutions

Graphic Packaging, Sonoco, and Smurfit Westrock highlighted sustainability-driven growth opportunities as core commercial strategies.

3. Packaging Is Outperforming Traditional Paper Markets

Consumer packaging remains significantly stronger than:

Printing papers

Commodity paperboard

Certain industrial paper grades

Companies with diversified packaging portfolios generally produced better operating results than pure paper producers.

EBITDA Performance Ranking

Top Tier

Packaging Corporation of America

Strong revenue growth

EBITDA approaching $500M

Acquisition synergies beginning to appear

Sonoco

$276.5M EBITDA

Strong productivity improvements

Significant margin resilience

Smurfit Westrock

Scale advantages

Global diversification

Packaging leadership

Middle Tier

Graphic Packaging

Revenue remained stable but EBITDA declined due to:

Pricing dislocation

Weather impacts

Inflation

Management's cost-reduction initiatives could improve margins during the second half of 2026.

Lower Tier

Clearwater Paper

Most challenged company in the group:

EBITDA collapsed from $30M to $2M

Severe pricing pressure

Negative earnings

Industry oversupply impacting profitability

Margin Expansion Leaders

1. Packaging Corporation of America

PCA delivered one of the strongest profitability profiles among peers due to:

Corrugated packaging strength

Operational efficiency

Acquisition integration

2. Sonoco

Management's profitability program is producing measurable results.

Target:

$150M–$200M savings over three years

3. Kimberly-Clark

Consumer brands continue providing pricing power unavailable to commodity producers.

Sustainability & Innovation Leaders

Gold Tier

Graphic Packaging

Most aggressive paper-for-plastic replacement strategy.

Highlights:

$15B addressable packaging opportunity

Multipack conversion

Paperboard containers

Recycled packaging expansion

Sonoco

Focus areas:

Paper can expansion

Sustainable consumer packaging

Asian growth investments

Smurfit Westrock

Global leadership in:

Circular packaging

Fiber-based solutions

Renewable materials

Companies Under Greatest Pressure

Clearwater Paper

Challenges:

7% pricing decline

EBITDA deterioration

Weather disruptions

Negative earnings

Recovery depends heavily on:

Industry capacity reductions

Demand normalization

Pricing recovery

Graphic Packaging

Despite strong strategic positioning:

Challenges:

EBITDA down significantly

Inflation pressure

Temporary pricing weakness

Long-term outlook remains favorable due to plastic replacement trends.

Strategic Themes Driving the Industry

AI Arrives in Paper Manufacturing

Several companies referenced:

AI procurement systems

Inventory optimization

Demand forecasting

Operational planning

Graphic Packaging has already deployed AI in procurement and inventory management.

This trend will likely accelerate across the industry.

Plastic Replacement Is Creating a Multi-Billion-Dollar Opportunity

One of the strongest themes across reports.

Applications include:

Food packaging

Beverage packaging

Consumer products

Foodservice

Graphic Packaging estimates approximately $15 billion in addressable market opportunities.

This may become the industry's most important growth driver during the next decade.

Debt Reduction Remains a Priority

Most management teams highlighted:

Cash preservation

Inventory reductions

Capital discipline

Rather than aggressive acquisitions, 2026 appears focused on:

Balance-sheet strengthening

Margin improvement

Free cash flow generation

2026 Industry Outlook

Bullish Factors

Plastic-to-paper conversion

Consumer packaging demand

Food and beverage resilience

AI-enabled productivity gains

Sustainability-driven innovation

Bearish Factors

Persistent inflation

Weak industrial demand

Pricing pressure

Global economic uncertainty

Trade policy and tariff risks

Industry Winners Heading Into H2 2026

Strongest Positioning

Packaging Corporation of America

Smurfit Westrock

Sonoco

Kimberly-Clark

International Paper

Most Attractive Transformation Story

Graphic Packaging

Highest Risk Profile

Clearwater Paper